Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

Europe's battery storage market is at a turning point. After years of rapid growth, the commercial landscape is becoming more complex, bringing new opportunities and new risks. As competition increases across ancillary services and wholesale markets, asset owners face a strategic question: how to structure bankable returns in a maturing market.

In this analysis, Synertics examines the commercial structures available to battery storage owners today: offtake agreements (physical tolls, floor agreements, revenue swaps), optimisation agreements for merchant operation, and co-location with renewables through hybrid PPAs. Each pathway offers distinct trade-offs between risk, reward, and operational control.

Battery energy storage systems (BESS) have become a core part of Europe's electricity grid. What started as pilot projects and residential solar-plus-storage has grown into a large-scale market where utility batteries now help manage renewable generation.

As wind and solar capacity expands, grids need more flexibility. Battery storage provides it by charging and discharging when it's economically most profitable, absorbing power when it's cheap and releasing it when high demand makes it valuable. In doing so, batteries also help keep the system stable.

According to SolarPower Europe's European Market Outlook for Battery Storage 2025-2029, (covering the EU 27 member states, the UK, and Switzerland) annual installations reached 21.9 GWh in 2024, bringing total installed capacity to 61.1 GWh. While this represents a 15% increase from 2023, the growth rate has significantly moderated. This slowdown reflects the easing of the energy crisis and the phase-out of emergency support schemes. In contrast, utility-scale projects continued to expand.

Looking ahead, the outlook remains strong. Under SolarPower Europe's medium scenario, annual installations are projected to reach nearly 120 GWh by 2029, bringing total installed capacity to approximately 400 GWh.

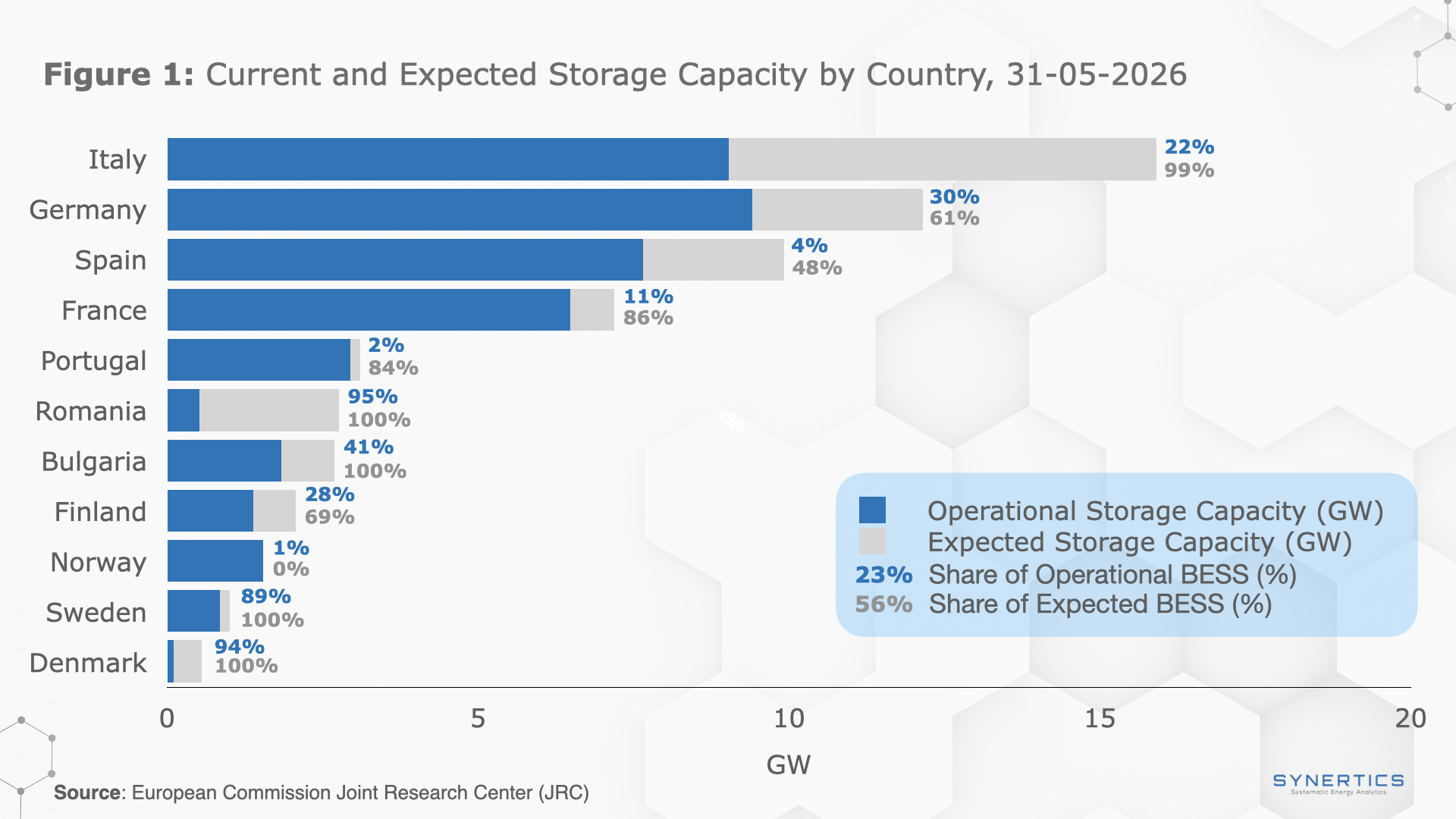

But this rapid build-out has a direct consequence. Europe’s battery fleet has expanded tenfold since 2020, bringing more competitiveness to ancillary services and wholesale markets (day-ahead, intraday).

A BESS offtake agreement is a contractual arrangement between a BESS asset owner and an offtaker (typically a utility or energy trader). Under this structure, the offtaker assumes partial or full exposure to market volatility in exchange for the right to optimise and monetise the battery’s operational flexibility. In return, the offtaker guarantees the owner a predictable revenue stream, a key requirement for securing project financing. The core variable in these agreements is the degree of risk transfer and the corresponding payment mechanism.

In the most fundamental structure, known as a physical toll, the offtaker assumes full market risk, capturing all upside from trading while absorbing any losses. In return for nomination and dispatch rights of the BESS asset, they pay the asset owner a fixed fee. This transfers both volatility and operational complexity to the offtaker, giving the owner predictable income regardless of market performance.

For asset owners seeking predictable revenue while retaining some exposure to market upside, a floor agreement offers a middle ground. In this structure, the offtaker guarantees the asset owner a minimum payment, the ‘floor’, and any revenue above that level is shared between the two parties according to an agreed split.

Not all offtake agreements involve physical control of the asset. A revenue swap is a type of financial derivative where the offtaker takes on market price risk, but the owner retains full operational control of the battery. The two parties agree on a fixed strike price and a reference index (typically the day-ahead market price). If the index price is below the strike, the offtaker pays the owner the difference. If it is above the strike, the owner pays the offtaker. The net effect is that the owner receives a predictable price for their electricity, regardless of market fluctuations. This makes revenue swaps a flexible tool for hedging price risk without surrendering control.

Not all asset owners enter into offtake agreements. An alternative is to retain full market exposure and operate the asset on a merchant basis. This means the owner takes on all market risk, keeping all revenue when prices are high but bearing the full impact when they are low. To handle bidding, dispatch, and trading, owners often work with a specialist optimiser that provides these services in exchange for a fee. There is no guaranteed revenue, but there is also no cap on upside. This approach suits investors with a higher risk appetite, though it can make project financing more challenging compared to structures with predictable income.

When a battery is built alongside a renewable plant (typically solar) the two assets can be marketed together under a single agreement known as a hybrid PPA.

In this structure, the battery's main job is to shape the renewable output. A solar PV asset without storage follows a bell curve: output rises through the morning, peaks at midday, and falls to zero in the evening. This concentration often depresses prices during peak generation hours, a phenomenon known as solar cannibalization. The battery addresses this by charging during low-price midday hours and discharging during the evening peak, when solar generation has faded but demand and prices remain high. This turns a variable solar profile into a firmer, more predictable product that better aligns with buyer consumption patterns.

This firming capability commands a clear financial upside. In a Synertics analysis of German PPA markets between September 2024 and September 2025, we found that solar-plus-storage PPAs consistently achieved prices approximately 20% higher than standalone solar PPAs over this period.

For the buyer, this premium is justified by avoided balancing costs and better alignment with actual consumption. For the seller and its financiers, the uplift improves project economics and supports a more bankable revenue stream, exactly the kind of predictable return that matters in a maturing market.

Hybrid PPAs do add complexity. They must balance the delivery of a shaped renewable profile with the flexibility to fully optimise the battery, and grid constraints in some European markets have limited adoption so far. But for co-located projects, they offer a way to combine revenue certainty with merchant upside in a single structure.

As European battery markets mature, the choice of agreement is no longer just a financial decision, it is a strategic one. Owners must weigh their need for revenue certainty against their appetite for risk and desire for control. Whether through the guaranteed income of a physical toll, the shared upside of a floor agreement, or the full exposure of merchant optimisation, the structures emerging today will shape how batteries are financed, built, and operated for years to come.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

4 min

Insights, Market-trends

12th Jun, 2026

8 min

Insights, Market-trends

11th Jun, 2026