Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

Since the end of 2025, the ancillary services landscape in Europe has changed. The Replacement Reserve market, a market that producers in Spain, Portugal and other European countries relied on to balance the grid and generate additional revenue, was discontinued on December 30th, 2025. With no centralized replacement planned, producers started looking at alternatives such as the intraday continuous market and the remaining balancing services, mFRR and aFRR. Greater competition in these markets is already starting to reshape volumes and prices.

In this analysis, Synertics examines how Spain and Portugal have adapted, comparing the first quarter of 2025, when RR was still active, against the first quarter of 2026 offering a clearer picture of what has changed and what to expect.

As the market works to integrate a higher share of renewables, operational changes have been necessary to better align the profile of renewable assets with the bidding periods available to producers.

One of the most significant recent shifts was the reduction of the cross-border intraday gate closure time, which passed from 60 minutes to 30 minutes, putting in practice since 14th of January 2026. By moving closer to real-time, solar and wind parks can now rely on later, more accurate weather forecasts. This directly helps decrease the financial risk of relying on early predictions and reduces the imbalances that occur between what was bidded and what is actually delivered to the grid.

While this change has provided a clear benefit to producers, such shifts usually mean that other sessions of the market are impacted. In this case, the Replacement Reserve (RR) in the ancillary services was discontinued. With hourly auctions settling the deliveries each 15-minute and a full activation time of up to 30 minutes, the market offered an additional revenue opportunity for flexible assets such as thermal generators, storage units, and some renewables that could meet the response time and commitment requirements of this slower-acting balancing product. Particularly as implemented through the TERRE platform, it was designed with a strong cross-border dimension in mind. Unlike aFRR and mFRR, which originated primarily as national or zonal products, the RR market was built around the idea of exchanging balancing energy between TSOs across different countries.

Which leads to the question: Where did this energy end up in 2026? Market participants have generally found alternatives like participating in the continuous intraday market for cross-border needs or most viable alternative for producers following the discontinuity of the RR has been to shift their flexibility into other balancing services, mFRR and aFRR. In the following sections, we will look at how these changes are playing out in the Iberian region and how they impact the performance of producers in the current market.

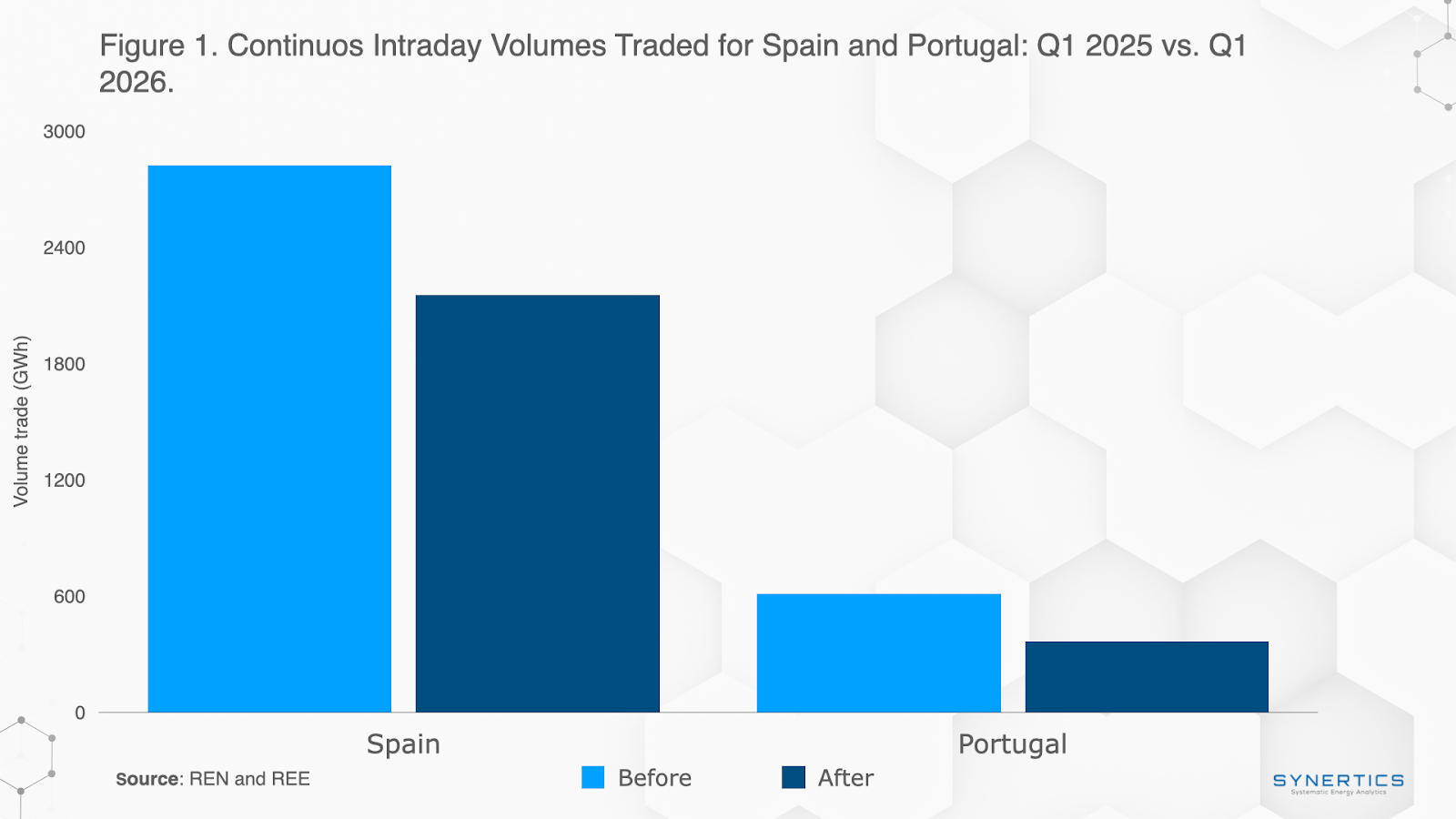

When analyzing cross-border energy exchange volumes, as shown in figures 1 and 2, the impact of RR discontinuation reveals interesting market dynamics. From figure 1, it can be seen that in the continuous intraday market a volume decreases, approximately 700 GWh for Spain and 300 GWh for Portugal in the first quarter (Q1) of 2026 compared with 2025. Although this would mean RR discontinuation led producers to move to other markets, such as single intraday sessions or balancing services. The numerous storms during Q1 2026, can be also the reason for smaller volumes during this quarter, because the unpredictive meteorological conditions reduced producers' participation in the market as they adopted more cautious market participations.

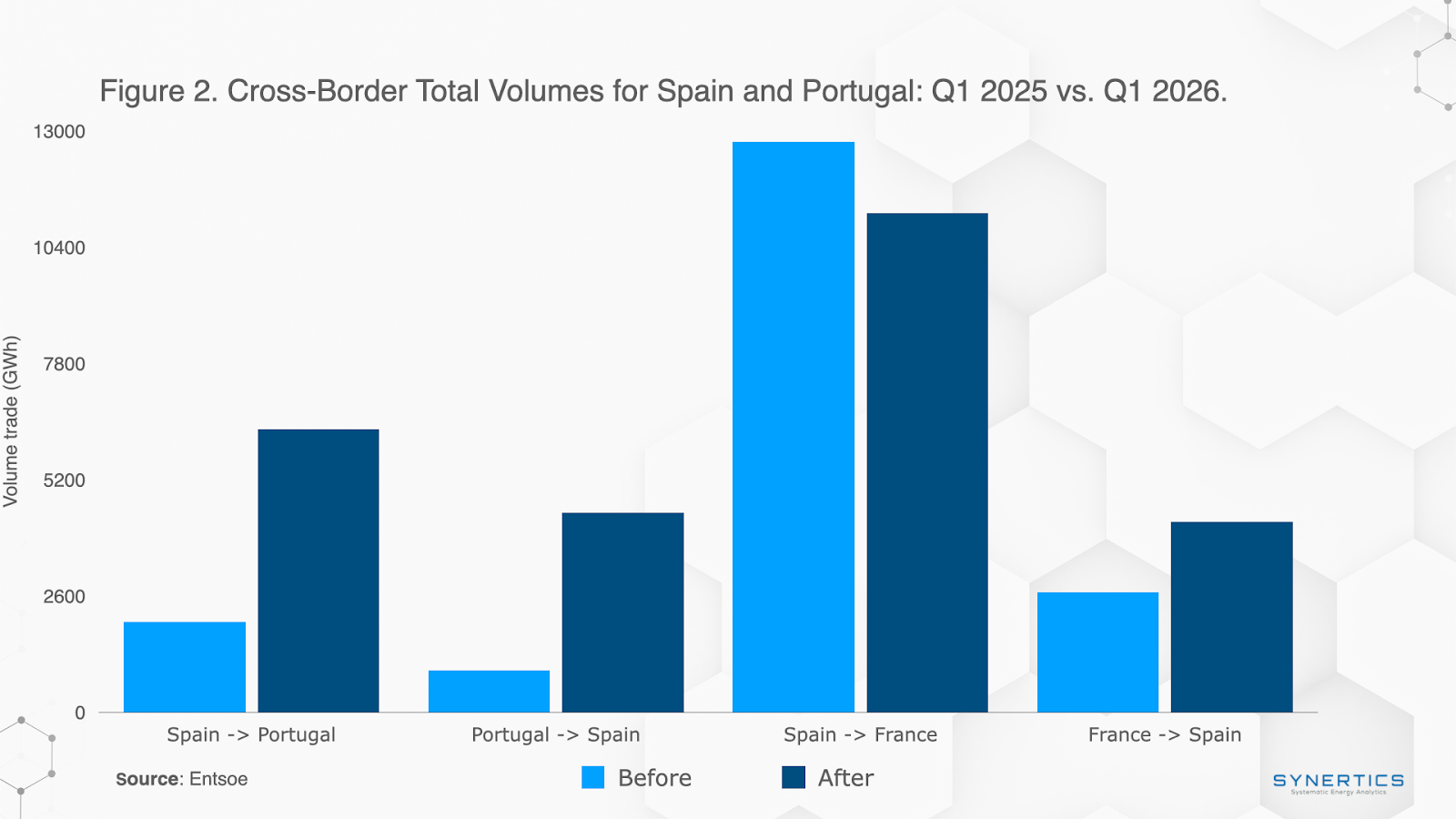

However, the total cross-border energy exchange between Portugal, Spain and France tells a different story. From figure 2, despite the SIDC continuous market decline, aggregate cross-border volumes increased in Q1 2026, particularly in Spain-Portugal. Spain to Portugal volumes increased from 2020 GWh to 6330 GWh and the other way around from 941 GWh to 4465 GWh. This increase can also be the impact of a bigger search in participating on the trans-european markets such as PICASSO (aFRR) and MARI (mFRR), where the next section will focus on how were the other ancillary services affected by this RR discontinuation.

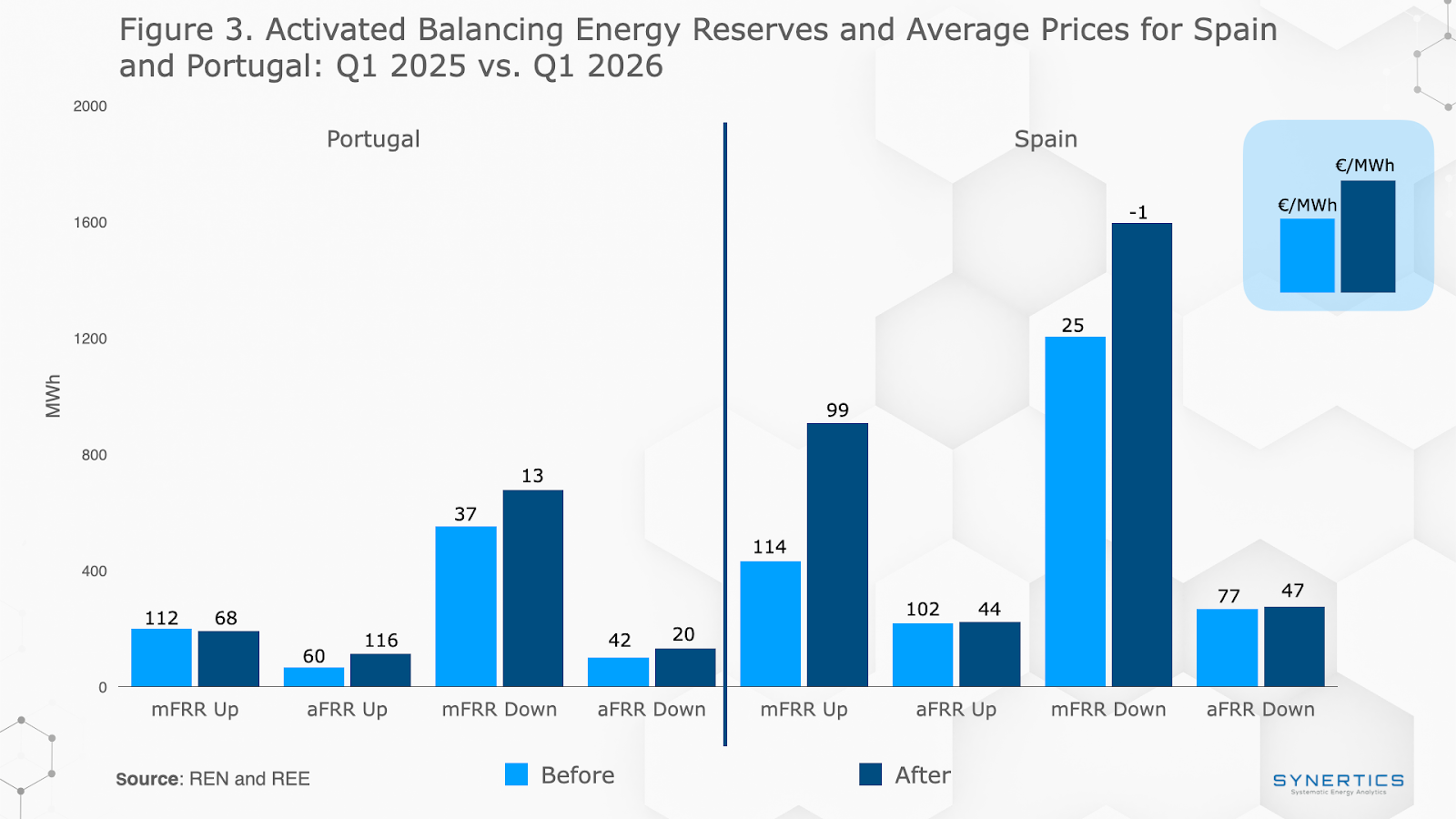

As illustrated in Figure 3, the activated volumes of the reserves, the mFRR market absorbed the most significant impact following the removal of the RR. As the immediate successor in the balancing timeframe, mFRR serves as the most natural technical substitute for the main participants of the RR market. The data indicates that the discontinuation of RR, rather than creating a capacity shortage, has accelerated the integration of Iberian balancing markets into the broader European framework.

As a major participant in both the RR and mFRR markets, Spain saw the most significant impact from the elimination of RR. Volumes surged while prices dropped, notably with the average price for mFRR down-regulation reaching -1.5 €/MWh. This indicates an environment where producers were willing to pay to curtail generation or consumers were compensated to increase their load. While the behavior was consistent across both markets, the intensity of the impact varied. In mFRR, volume growth outpaced price declines, suggesting that traditional RR participants (excluding renewables) migrated to this market to capture extra profit. Meanwhile, renewable producers might have shifted their focus to aFRR due to its faster response times. This influx of renewable supply, combined with the integration of the PICASSO platform, increased competition and caused aFRR prices to decrease more sharply than those in mFRR.

A similar behaviour can be seen in Portugal. Regarding the prices, only aFRR up regulation went higher when comparing with Q1 2025, as this might be the effect of the small competition that exists between Balancing service providers (BSP) to balance the grid, with the impact of storms in the weather conditions a bigger and quick fix might have been needed. For the mFRR market the volumes didn’t increase as much since the small competitions might have helped to not have a big increase of participation.

This migration has introduced new commercial challenges for producers. As the current mFRR and aFRR frameworks are more inclusive for renewable assets and the RR process is phased out, competition for balancing services has intensified. The expanded capacity to supply these smaller adjustment services means renewable producers face a higher risk of having their offers rejected.

As the Replacement Reserve served as a long-duration balancing service, its discontinuity has primarily impacted other ancillary services, most notably mFRR in Spain. Comparing the first quarter of 2025 to 2026, average prices shifted drastically from 25.37 to -1.5 €/MWh. Given that Spain was historically one of the largest contributors to the RR market, this price volatility has been significantly more pronounced there than in Portugal.

For solar and wind parks, this influx of new competition into the mFRR and aFRR markets points toward a new reality of declining margins as prices and cleared volumes decline. As balancing services become less lucrative due to increased saturation, renewable producers may choose to mitigate more of their energy through the intraday market. This strategy has become a primary focus since 2025, as the shift from hourly to 15-minute bidding resolutions allows for much finer portfolio adjustments closer to real-time.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

3 min

Insights, Announcements

29th Jul, 2026