Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

Battery energy storage is increasingly framed as the technology that will eventually displace peak gas and oil generation in European power systems. The pace of buildout has accelerated across most major markets, supported by capacity-market revenues, government subsidies, and dedicated long-term auctions such as Italy’s MACSE programme.

How much of the current peaking burden can today’s BESS fleet realistically displace, and how much remains uncovered once the committed pipeline is delivered? In this analysis, Synertics compares the maximum coincident gas and oil generation observed at the moment of system peak in six European markets against operational BESS capacity and the committed project pipeline, identifying the coverage achievable today and the coverage achievable once committed projects are built.

There are several ways to define the volume of fossil peaking generation that BESS would need to replace. We did not use total installed gas and oil nameplate capacity, as it overstates the flexibility the system relies on in practice. A country can have 40 GW of thermal capacity on its books and rarely dispatch more than half of it simultaneously.

Instead, for each market we identified the single timestamp at which coincident gas-plus-oil generation reached its observed maximum and used that dispatched volume as the reference quantity. This represents the volume of gas and oil generation the system dispatched at its peak moment over the observation period. In Germany, for example, installed gas and oil capacity stands close to 39.5 GW, but coincident dispatch peaked at 21.0 GW on 15 January 2025 at 17:45. The 21.0 GW figure, not the 39.5 GW nameplate, is used as the reference.

This peak generation value is then compared against two measures of battery readiness. The first is operational BESS capacity, the share of peak gas and oil generation already covered by energised assets today. The second is the committed BESS pipeline, defined here as projects under construction or with permits secured. Early-stage announced capacity is excluded from this figure, given the high attrition rate between announcement and delivery.

The data is drawn from ENTSO-E and the European Commission Joint Research Centre. The analysis covers six European markets: Italy, Germany, Spain, the Netherlands, France and Poland.

One methodological caveat applies throughout. The comparison is based on power capacity (MW), not energy (MWh). Matching peak generation on a power basis is the first step; covering the duration of the peak is a separate question, returned to in the closing section.

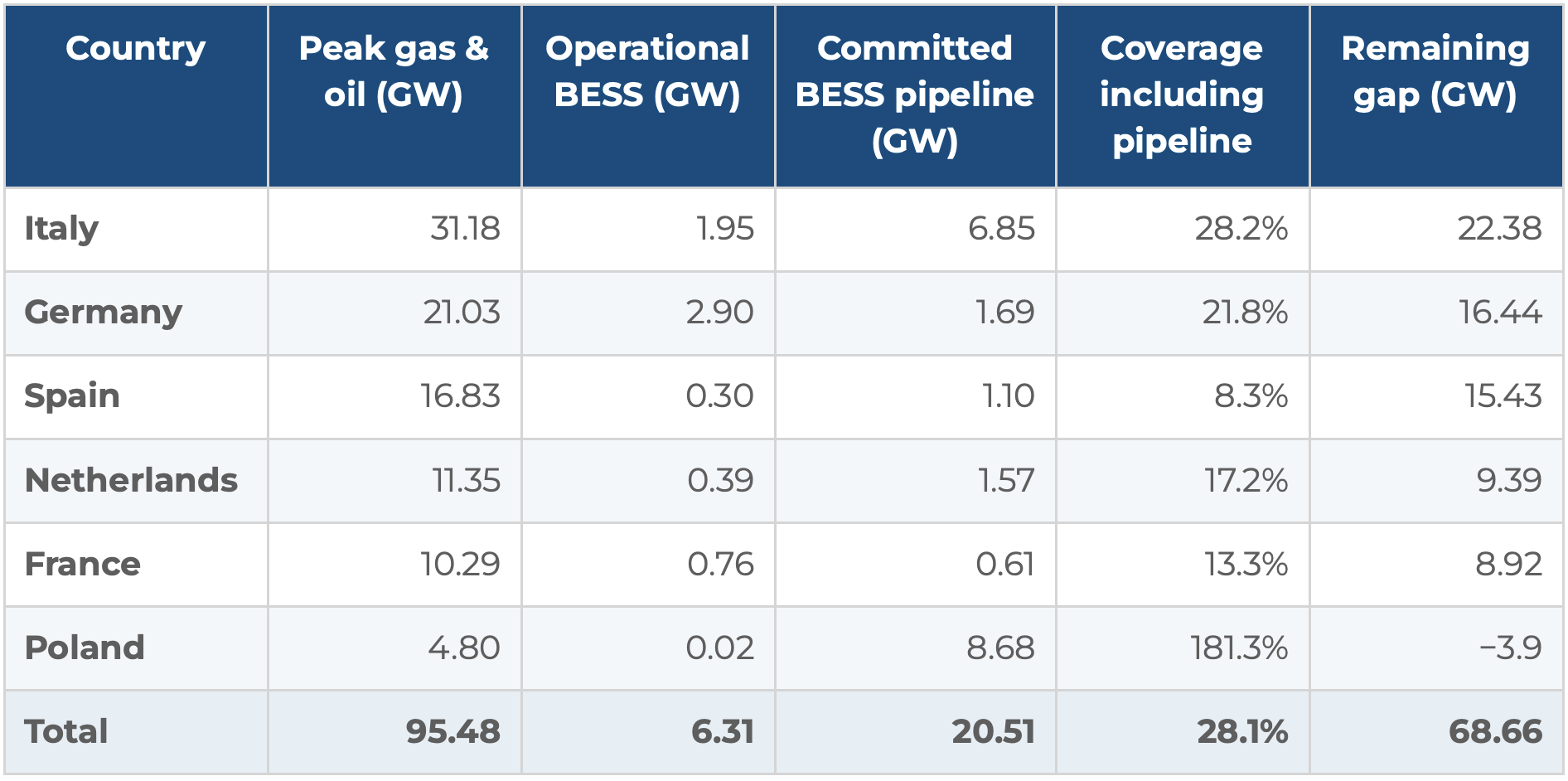

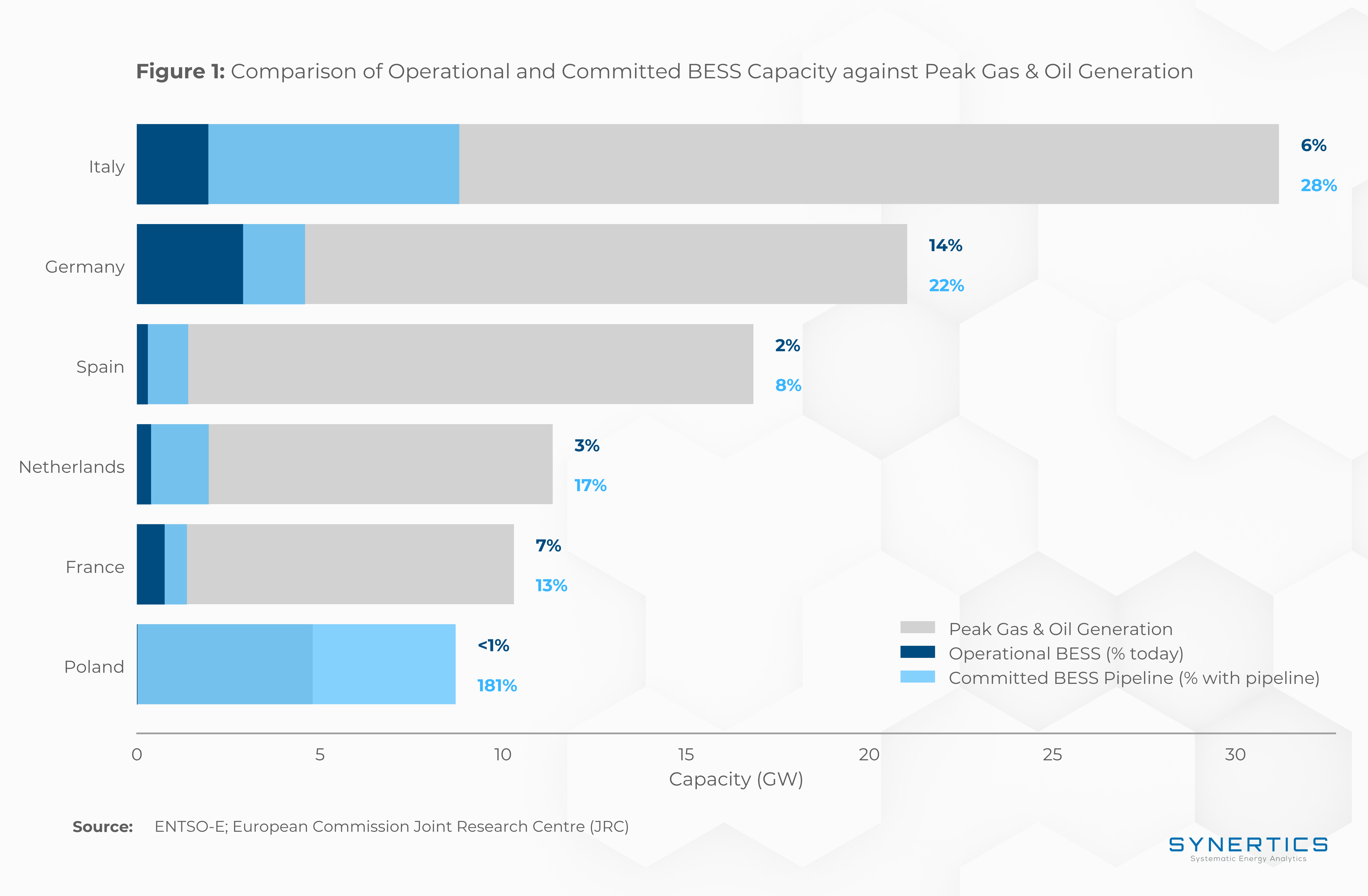

Across the six markets, observed peak gas and oil generation totals approximately 95.5 GW. Operational BESS currently covers 6.6% of this figure. Once the committed pipeline is delivered, coverage rises to 28.1%, leaving a residual gap of approximately 68.7 GW. To fully offset coincident peak gas and oil generation on a power basis, the operational fleet would need to grow by a factor close to 15 times across this set of markets.

Source: ENTSO-E and European Commission Joint Research Centre data, 2026.

Italy records the highest peak gas and oil generation in the set at 31.2 GW, reflecting a generation mix in which gas remains the dominant flexible source. Operational BESS stands at 2.0 GW (6% of peak), with a further 6.9 GW in the committed pipeline. With the pipeline delivered, coverage would reach 28% of peak. Italy’s forward trajectory is supported by Terna’s MACSE auction, whose first round in September 2025 awarded 1.5 GW of BESS capacity (15 projects, average duration 6.6 hours) on 15-year tolling contracts. The auction cleared at an average price of approximately €13,000/MWh per year, against a reserve price of €37,000/MWh per year set by the regulator.

Germany records the second-largest peak gas and oil generation in the set at 21.0 GW. Operational BESS stands at 2.9 GW (14% of peak), the largest operational fleet among the markets analysed; Germany also led Europe in total new battery storage installations in 2024. The committed pipeline of 1.7 GW would lift coverage to 22% of peak. A national capacity market that will include storage among eligible technologies is in preparation and is expected to become operational in 2028.

Spain combines the third-largest peak gas and oil generation in the set (16.8 GW) with one of the smallest operational fleets (0.3 GW, 2% of peak). The committed pipeline of 1.1 GW would lift coverage to 8%, the lowest among the markets analysed. Following the April 2025 blackout, the Spanish government has introduced a €700 million support programme and announced a 2030 energy storage target above 20 GW. Curtailment of renewable generation has been material in recent months, increasing the focus on flexibility build-out.

The Netherlands records 11.3 GW of peak gas and oil generation, reflecting a generation system long anchored in gas. Operational BESS stands at 0.4 GW (3% of peak), with 1.6 GW committed; coverage rises to 17% with the pipeline delivered. Severe grid congestion is the principal driver of battery storage demand in the Netherlands. In late 2025, TenneT confirmed grid access for around 6 GW of battery projects through new time-dependent transmission right contracts. Separately, the ACM has introduced a prioritisation framework allowing projects qualifying as congestion mitigators to advance in the connection queue.

France records 10.3 GW of peak gas and oil generation, a relatively modest figure given the size of the system, reflecting the dominance of nuclear baseload. Operational BESS stands at 0.8 GW (7% of peak), with 0.6 GW committed; coverage rises to 13% with the pipeline delivered. Revenue for these assets is currently split between merchant markets and the French Capacity Mechanism. A 10-year centralized reform of this mechanism was approved by the European Commission in December 2025, with the first major auctions for the 2026–2036 period scheduled for July 2026.

Poland is the outlier among the markets analysed. Peak gas and oil generation of 4.8 GW is the smallest in the set, while the committed pipeline of 8.7 GW is the largest. This pipeline represents 181% of the observed gas and oil peak, a volume driven by the Polish capacity-market auctions. This surplus relative to gas and oil capacity reflects a broader systemic shift, where BESS is being deployed not only to offset gas peaking but to provide the flexibility required to facilitate the phase-out of the country's coal-fired generation. As operational BESS today is only 17 MW, the trajectory depends entirely on the delivery of this contracted pipeline.

The coverage figures above are based on power capacity (MW), comparing BESS power against peak gas and oil generation at the moment of observed system peak. They do not capture the energy dimension.

A gas turbine can run for as long as it is fuelled. A battery discharges only until it is empty. The peaks captured in the dataset are not instantaneous spikes; they are sustained evening ramps lasting several hours. The MACSE projects in Italy were procured at an average duration of 6.6 hours, reflecting an auction structure that rewards longer-duration assets capable of holding the system through the full evening ramp. A fleet sized to match power on a coincident basis using two-hour batteries would still fall short on energy when the peak runs long.

For this reason, the 68.7 GW residual power gap identified above should be treated as a floor on the build-out required to fully displace peak gas and oil generation. Closing the gap on a power basis is necessary; achieving the same outcome on an energy basis requires both more megawatts and longer-duration assets.

Beyond the national capacity gaps, the commercial strategy for individual assets is driven by arbitrage: the ability to store low-price midday energy and sell it during high-price evening windows. This necessity is dictated by the current merit order, as long as gas and oil units are required to meet evening peak demand, batteries can displace them by discharging lower-cost stored surplus.

The most sensible configuration today pairs a renewable plant with a battery of equal power capacity and four hours of duration, for example, a 10 MW solar farm with a 10 MW / 40 MWh BESS. This allows the asset to store midday surplus, when grid congestion or oversupply depresses prices, and time-shift that energy to the evening peak. A shorter-duration battery would empty before the highest evening price spikes are reached, failing to capture the full daily price spread or to fully displace thermal units that remain active throughout the peak. For larger installations, the battery is often sized at half the renewable plant's power capacity (e.g. a 100 MW solar farm with a 50 MW / 200 MWh BESS) to optimise capital expenditure, while four-hour duration remains the benchmark for bankability across the markets analysed.

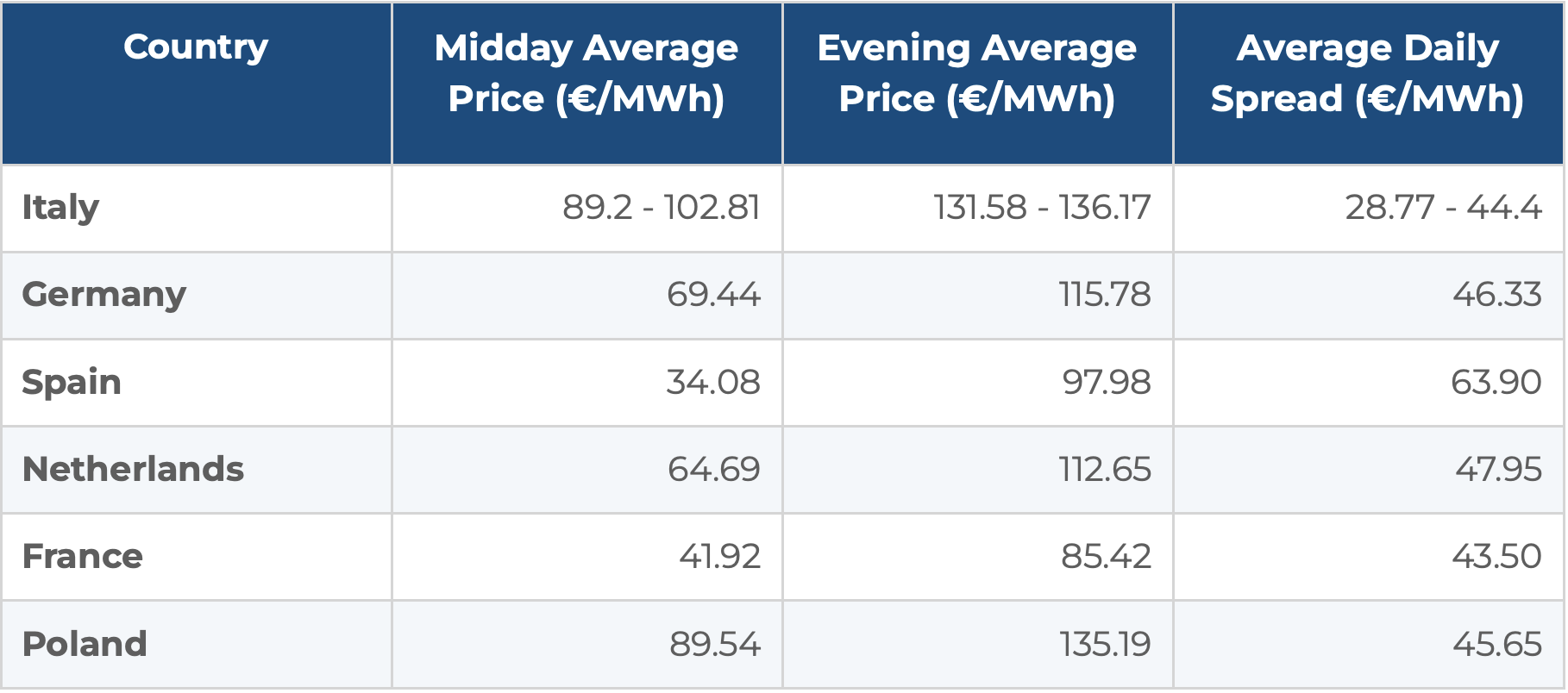

While the technical imperative for BESS is defined by the displacement of fossil-fuel peaker plants, its commercial viability is anchored in daily price volatility. To quantify this opportunity, we conducted a granular analysis of 2025 Day-Ahead market data, identifying a persistent 'Arbitrage Gap' across the target European cluster. By benchmarking a standard 4-hour discharge profile, aligning midday charging cycles with evening demand peaks, we have validated the revenue-capture potential essential for a bankable investment case.

Source: ENTSO-E

In Italy, the arbitrage potential is highly location-dependent. While the industrial North maintains a flatter profile with spreads of €28.77, the Southern and Island zones (Sicily and Sardinia) deliver spreads as high as €44.40. This divergence is driven by localized solar saturation and grid congestion, making strategic site selection in the South critical for maximizing project returns.

Across the broader cluster, Spain leads with a €63.90 spread due to its deep midday price troughs, while the highly integrated German, Dutch, and French markets maintain consistent spreads in the €43–€48 range. In Poland and Northern Italy, midday prices remain higher due to thermal baseload reliance; however, as solar capacity increases through 2026, we expect these midday "floors" to drop, further widening the available arbitrage gap.

The 4-hour discharge duration is the optimal configuration to capture this volatility. Across all six markets, the evening peak window consistently spans three to five hours, making a 4-hour BESS the most effective duration to maximize energy volume during these high-value periods. This configuration ensures the asset captures the bulk of the daily price delta, providing the financial resilience required for large-scale investment.

Across the six markets analysed, operational BESS currently covers 6.6% of observed peak gas and oil generation, rising to 28.1% once the committed pipeline is delivered. This trajectory varies materially by market. Italy and Poland lead in forward coverage through centralized procurement with firm delivery obligations, while other markets are currently transitioning from merchant-driven models toward long-term capacity frameworks to close their respective gaps.

This leaves a 68.7 GW residual power gap. To fully displace this fossil capacity, the build-out must not only match the peak power but also provide sufficient duration, typically estimated at four hours of continuous discharge. On this basis, the total energy storage requirement across these six markets stands at approximately 275 GWh to ensure the system remains balanced through the full duration of a winter evening peak.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

4 min

Insights, Market-trends

12th Jun, 2026

8 min

Insights, Market-trends

11th Jun, 2026