Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

Battery energy storage is increasingly seen as a key tool for integrating wind and solar into European power systems. As renewable capacity grows, so does the need for flexible resources that can absorb excess generation and deliver power when the sun is not shining and the wind is not blowing. Yet the pace of battery deployment across Europe tells a fragmented story: some markets have built significant capacity while others, despite strong renewable growth, have barely started.

In this analysis, Synertics examines the relationship between energy storage deployment and day-ahead price volatility across eleven European markets. Using operational capacity, pipeline data and wholesale price spreads, the analysis assesses whether countries with greater storage coverage relative to their renewable output show structurally lower price volatility or whether other factors run deep enough that storage alone is not yet sufficient to compress it.

As renewable capacity has expanded across Europe, near-zero and negative price events during daylight hours have become more frequent, precisely the window when solar parks generate the most power. This has pushed producers to look for ways to capture value outside those low-price hours, with Battery Energy Storage Systems (BESS) emerging as one of the most direct commercial responses, capturing the spread between low and high price hours while also providing ancillary services to the grid.

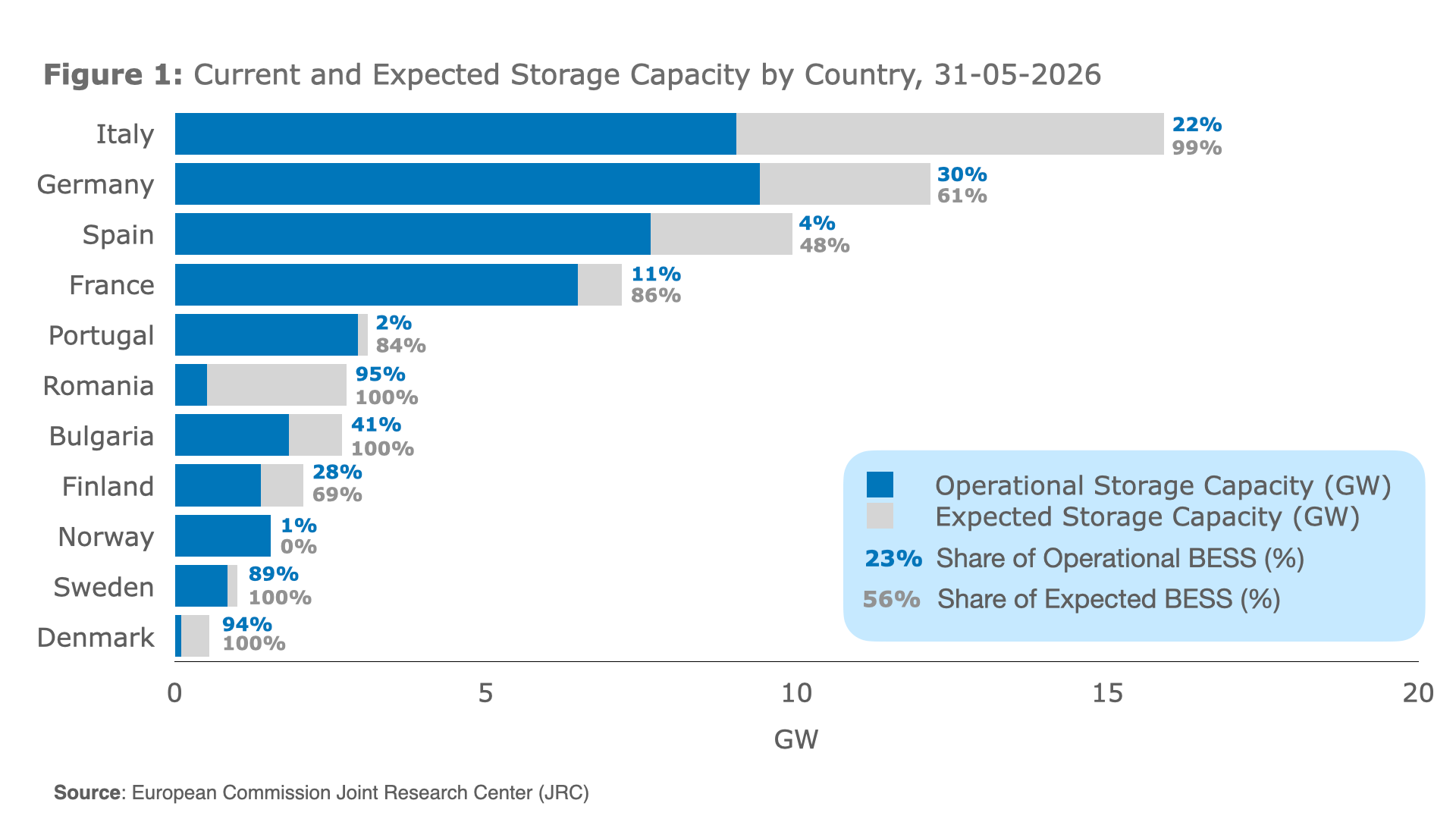

Figure 1 shows where each country currently stands and where the storage capacity is heading. Looking at the expected pipeline, it can be seen that there is the tendency for all the countries to increase their storage capacity with batteries, especially Italy, Germany and Spain are the markets with the largest committed expansions ahead, with Italy approaching a major expansion of its current operational fleet driven by the MACSE auction programme. Romania already has operational fleets in place but still have the majority of their future capacity in development. Among the countries where BESS deployment is already most advanced relative to their total expected capacity, Denmark leads with 94% of its pipeline already operational, followed closely by Sweden at 89%, though both operate at a smaller absolute scale compared to the larger markets.

To assess if the storage capacity of a country has any impact on the energy price volatility across European markets, two indicators were used:

Together these two metrics describe both the magnitude and the consistency of price volatility each market experiences.

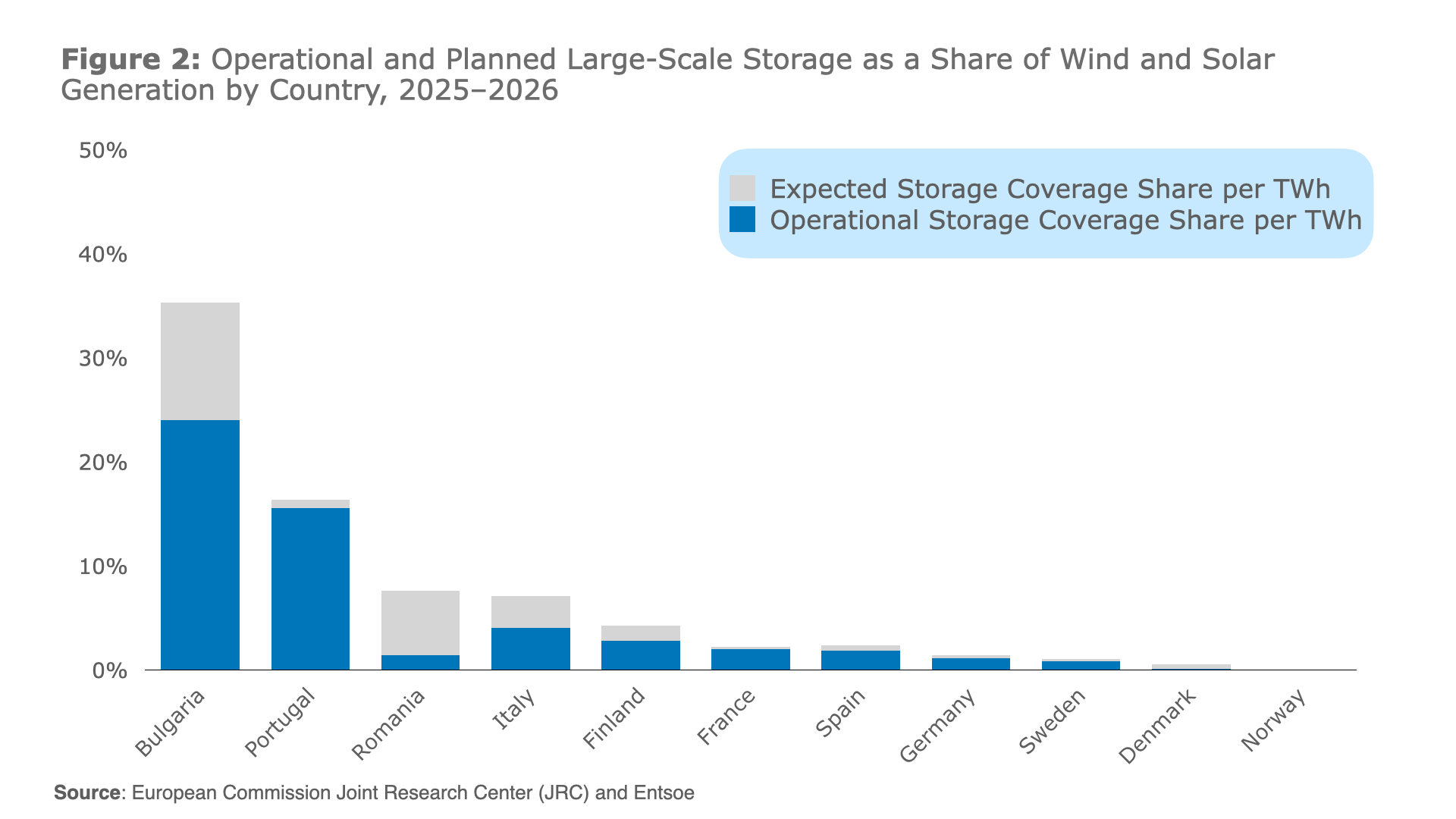

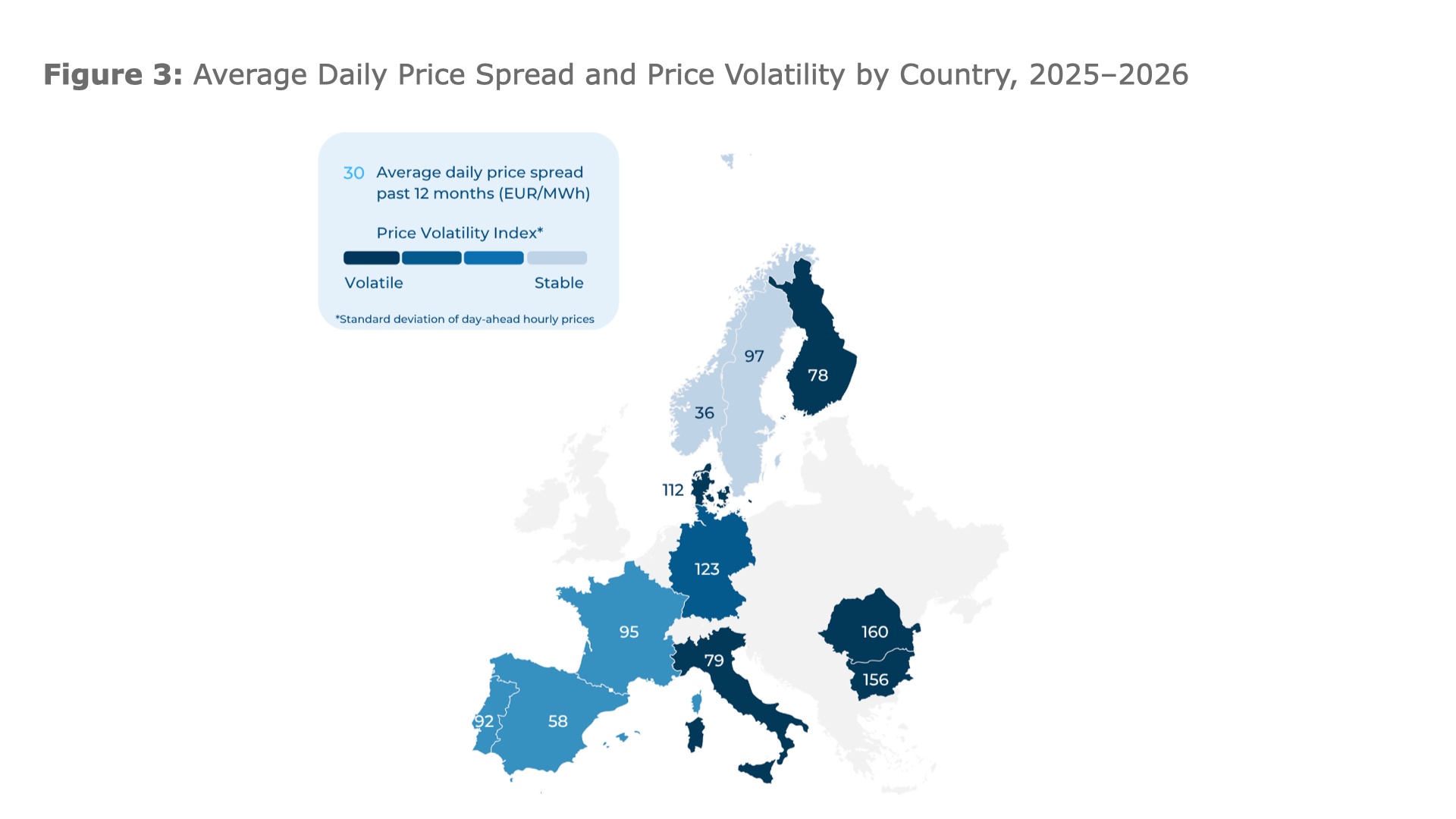

Figure 2 and Figure 3 together illustrate this relationship across European markets, combining the renewable storage coverage of existing and planned capacity with the price volatility each market recorded over the observation period. The picture varies considerably by country, pointing to structural differences in how storage deployment has shaped, or has yet to shape, price behaviour.

Eastern Europe

Romania and Bulgaria record the highest price volatility in the dataset, with average daily spreads of 156 and 160 EUR/MWh reflecting persistent structural imbalances driven by limited interconnection and a generation mix still transitioning away from thermal sources. The contrast between the two in Figure 2 is notable. Bulgaria has the highest storage coverage ratio in the dataset, with operational BESS already covering around 25% of its wind and solar output and a committed pipeline taking that figure to approximately 35%, yet Bulgaria remains one of the most price-volatile markets in the dataset, with a spread of 160 EUR/MWh and a price volatility index that confirms this is a persistent structural feature rather than an occasional spike. This is one of the clearest findings in the analysis: even at 25% operational coverage, the highest in the dataset, storage has not been sufficient to compress prices. The grid constraints driving volatility in Bulgaria are structural, rooted in limited interconnection capacity with neighbouring markets and cannot be resolved by storage deployment alone.

Romania, despite similar volatility levels, has barely begun deploying operational capacity, with coverage close to 1% today and a pipeline that would bring it to around 7%, leaving the underlying price instability largely unaddressed by storage for now.

Central Europe

Germany and France present a different profile. Both markets show moderate but consistent price spreads, 123 EUR/MWh in Germany and 95 EUR/MWh in France and as Figure 2 shows, operational storage coverage remains below 5% in both countries relative to the scale of their renewable fleets. Figure 3 reflects higher price volatility in Germany than in France, consistent with a generation mix increasingly dominated by variable wind and solar. According to Fraunhofer ISE, wind and solar together accounted for over 65% of German public electricity generation in 2025, while storage deployment has not kept pace with that growth. France benefits from nuclear baseload reducing the frequency of extreme price events, but its renewable expansion is accelerating and the coverage ratio tells a similar story. In both markets the gap between renewable output and storage capacity continues to widen and the regulatory frameworks are moving in a supportive direction, with France advancing reforms to its capacity market and Germany introducing bridging capacity auctions from 2027 and a full capacity market expected from 2032.

Southern Europe

Italy's large announced pipeline, driven by the MACSE auction programme, would push its coverage from around 5% today to roughly 7%, a modest shift in relative terms despite being the largest pipeline in Europe in absolute GW. The limited impact on coverage reflects the scale of Italy's renewable fleet, but the more structural issue is geographic. Renewable energy production is concentrated in the south while electricity demand remains anchored in the industrial north and the resulting congestion limits the flow of clean power and increases system costs. This is precisely what MACSE is designed to address: the first auction procured 10 GWh exclusively in Southern Italy and the islands, and the full pipeline concentrates most of its capacity in the same zones, with 16.8 GWh in the South, 13.6 GWh in Sicily and 10.4 GWh in Sardinia.

Portugal and Spain present an interesting contrast within the Iberian peninsula. Portugal stands out in Figure 2 as the second highest coverage ratio in the dataset at around 16% operational, with very little additional pipeline committed, yet it records a spread of 92 EUR/MWh, higher than Spain at 58 EUR/MWh which has an operational coverage ratio below 2% and a limited pipeline. Spain's lower volatility relative to its renewable penetration reflects the maturity and interconnection of the Iberian market rather than storage deployment. Portugal's higher spread despite greater storage coverage points to the limits of storage as the sole driver of volatility, with price dynamics also shaped by its relatively narrow revenue stack and limited interconnection with the broader peninsula.

Northern Europe

The Nordic region presents two distinct profiles. On one side, Norway, where price stability is driven by structural factors rather than storage deployment and Sweden, where a meaningful coverage ratio has already been built but the marginal case for further investment is narrowing. On the other, Denmark and Finland, where higher wind penetration creates more frequent price swings but alternative flexibility solutions limit the case for large-scale battery investment.

Norway generates most of its electricity from hydropower, providing an inherent flexibility that removes the need for battery-based balancing. Figure 2 confirms this with a coverage ratio close to zero and no meaningful pipeline in development. For Sweden, a higher spread of 97 EUR/MWh can be seen, driven by growing wind capacity, but has already built a meaningful coverage ratio through ancillary service revenues. With those markets maturing, the case for significant new BESS investment in Sweden is narrowing.

Denmark depends a lot on wind to generate its electricity, which combined with strong interconnection to neighbouring markets produces a spread of 112 EUR/MWh. The grid's export capacity, however, limits the structural need for domestic storage to absorb surplus generation. Finland records a spread of 78 EUR/MWh and has been one of the more active Nordic markets for BESS investment, supported by highly volatile day-ahead prices and tax exemptions for new storage projects.

This analysis shows that storage capacity has a measurable impact on day-ahead price volatility, but is not the dominant factor in most markets examined. Bulgaria is the clearest example: the highest storage coverage in the dataset at around 25% operational, yet one of the most volatile markets in Europe, demonstrating that where grid constraints and limited interconnection are the structural drivers of volatility, storage alone cannot compress them. In markets where variable renewable generation is the primary source of price instability, such as Germany and Italy, the pipelines being built today are more likely to translate into lower volatility as they are commissioned. The broader finding is that storage is one lever among several and its impact on price dynamics depends as much on the grid infrastructure and market design surrounding it as on the volume of capacity deployed.

3- https://ratedpower.com/blog/utility-sacle-storage-italy/

13 min

13 min

Insights

16th Jul, 2026

4 min

Insights, Market-trends

12th Jun, 2026

4 min

Insights, Market-trends

12th Jun, 2026