Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

As the winter season draws to a close, energy producers across Europe have faced a series of market events with results varying sharply by the country they participate in. As we covered in our January and February News Round-Ups, the energy landscape has been volatile. From the historic milestone of wind and solar power surpassing fossil fuels, to price volatility driven by severe storms in the South and a persistent wind drought combined with dry conditions in the North. These developments have left producers questioning whether such market fluctuations are temporary anomalies or a new, more challenging baseline.

In this post, Synertics analyses this past winter's performance against historical data to assess whether these market shifts represent a temporary phase or a lasting revenue risk.

For this analysis, Synertics utilizes countries technology specific generation and meteorological data to evaluate how rainfall, wind gusts and irradiance shaped market participation. By benchmarking this winter against the two-year average (2023/24 and 2024/25), we focus on the countries that experienced the most significant impacts, identifying where asset owners captured low capture prices and where they faced heightened imbalance risks.

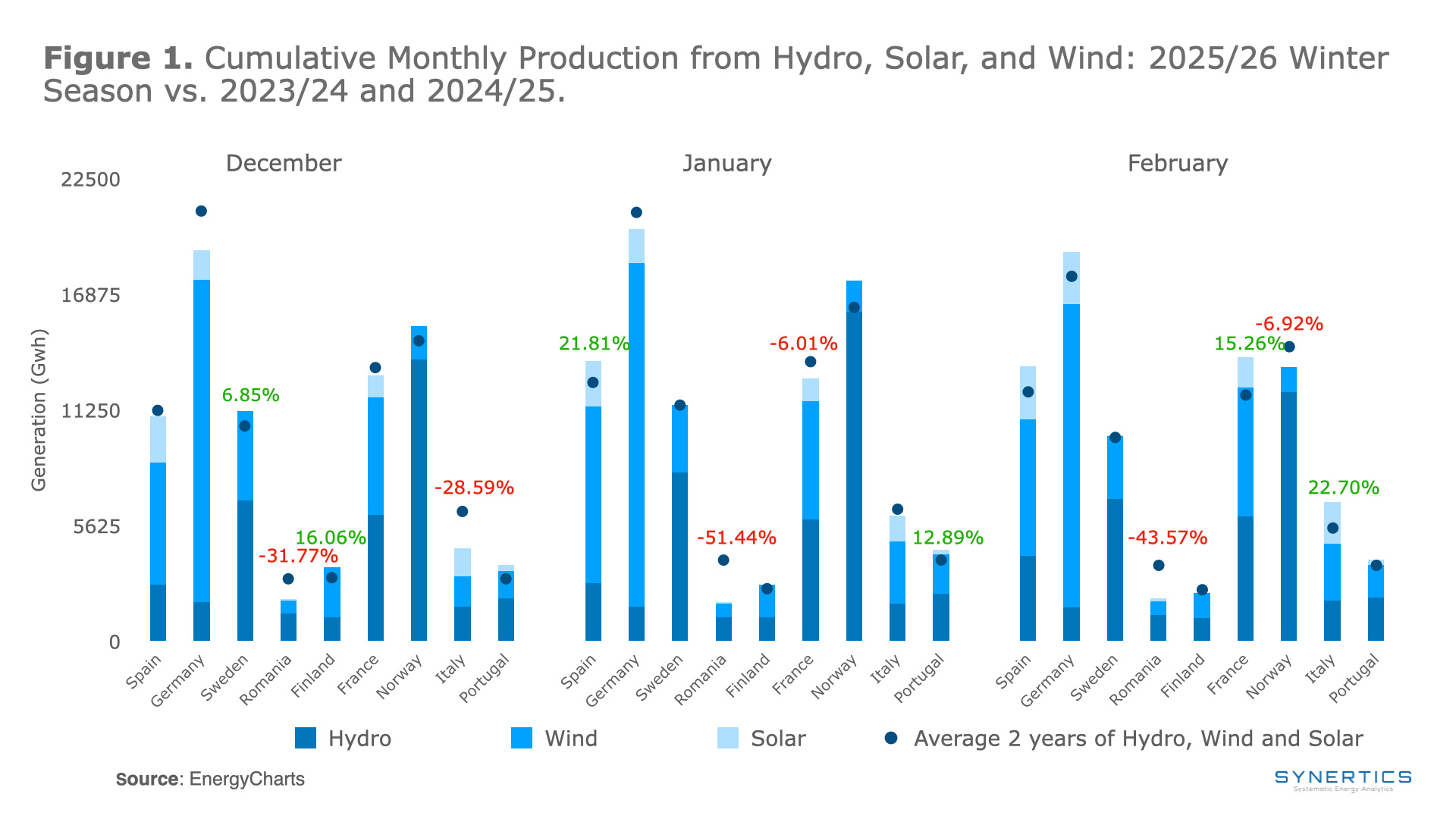

Figure 1 shows cumulative renewable generation across nine representative European markets for the 2025/26 winter against two-year historical average. While overall generation exceeded historical levels, regional exceptions highlight the distinct impact of local weather patterns and market evolution.

The standout was the Southern region, where a succession of Atlantic storms through January and February drove both wind and hydro generation well above seasonal norms. Continuous rainfall pushed reservoirs to high storage levels and with both technologies carrying near-zero marginal costs, their combined surge put consistent downward pressure on market prices, a dynamic that did not go unnoticed by other market participants. We see that first was Spain and Portugal with values above 21% and 12% respectively in January and in February, Italy and France as respectively surpassed their two winter averages by 15.26% and 22.70%.

Romania was the winter's biggest outlier, with January production dropping 50% below average. While low wind and water levels played a part, the energy system is also changing. Transelectrica reports show that grid demand is falling because home solar (prosumers) grew by 45% in one year and businesses have become much more energy-efficient since the 2022 energy crisis. Regarding the Nordic region, despite the wind drought and dry conditions, deviations remained comparatively contained. The presence of nuclear capacity in markets like Finland and Sweden reduces grid dependence on renewables, providing a stable baseload that mitigated the impact of a weaker renewable season.

Germany presents a neutral winter: a weak December driven by a wind drought followed by a strong recovery in January and February, consistent with the volatility patterns flagged in our earlier round-ups.

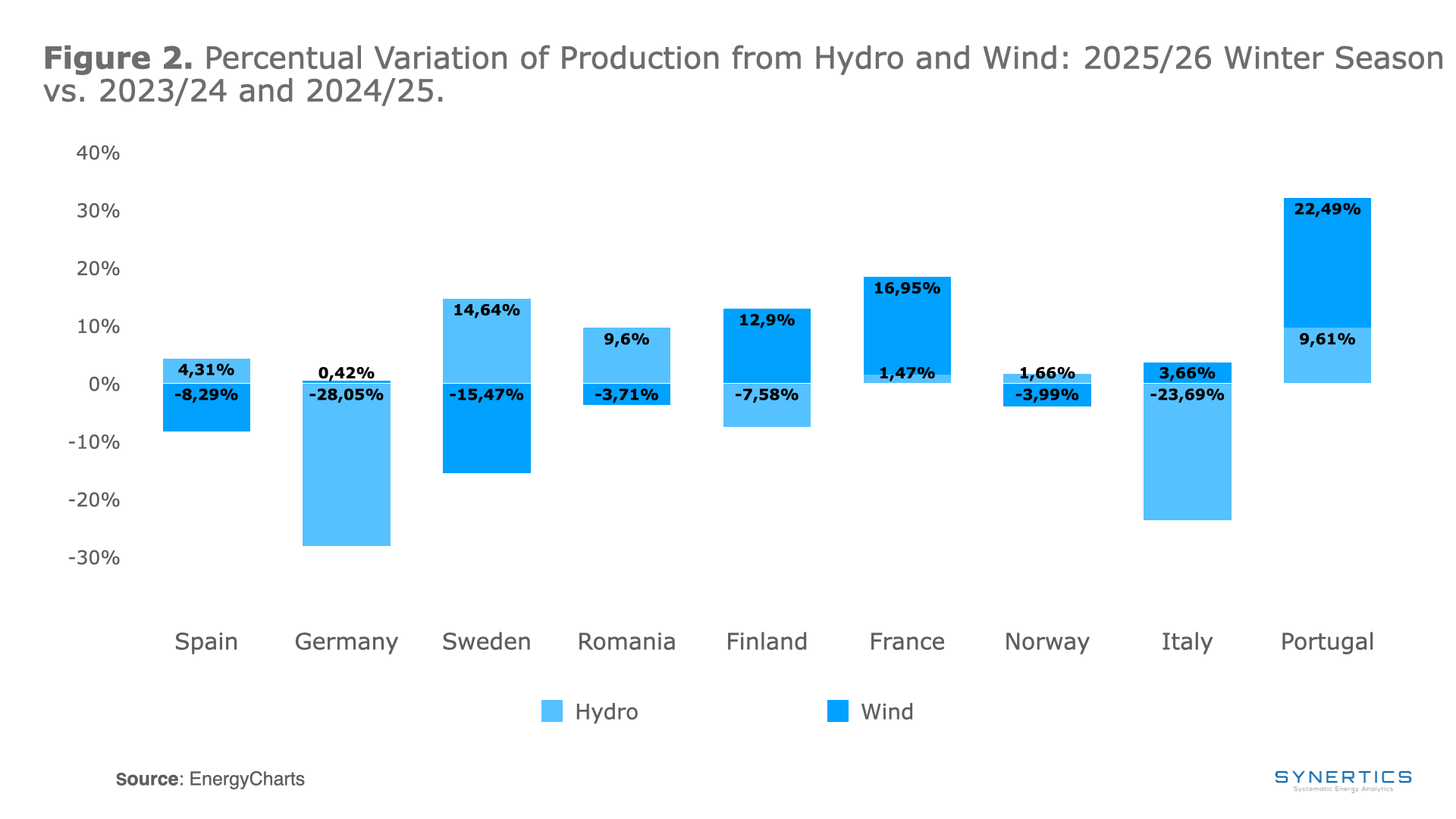

Despite rapid capacity growth, solar remains a secondary winter contributor due to seasonal light constraints. Wind and hydro continue to carry the seasonal load, though their risk profiles differ significantly: while hydropower offers controllable dispatch, wind generation depends entirely on the weather. Figure 2 isolates the percentual variation in wind and hydro generation individually against the 2023–2025 benchmark and the contrast between the two technologies is hard to ignore.

Hydro outperformed notably in Portugal, Romania and Sweden. In Portugal (9.61%), continuous rainfall forced reservoirs to discharge to maintain safety limits. In Sweden (14.64%) hydro was ramped up to cover the deficit from a persistent wind drought. Romania's 9.6% hydro outperformance was a result of high reservoir starting levels and the dams' critical role in balancing the grid during the regional wind drought. Conversely, performance fell short in Germany (-28.05%), Finland (-7.58%), and Italy (-23.69%) due to possible precipitation deficit and low Alpine snowpack. Meanwhile, Finland was constrained by the 'dry North' conditions, where, unlike Sweden, reservoir levels were too low to sustain higher generation during the wind drought.

Regarding wind, it is important to note that Sweden and Spain underperformed by -15.47% and -8.29%, respectively, as they were hit by prolonged high-pressure blocking systems that created wind droughts, stalling turbines for weeks. Conversely, Portugal (22.49%), France (16.95%), and Finland (12.95%) saw significant increases compared to the last two years. This was due to an active Atlantic storm track that directed a series of powerful low-pressure systems (such as Storms Kristin and Leonardo) across the West, while a stronger-than-average jet stream boosted wind speeds across the Baltic and Nordic regions.

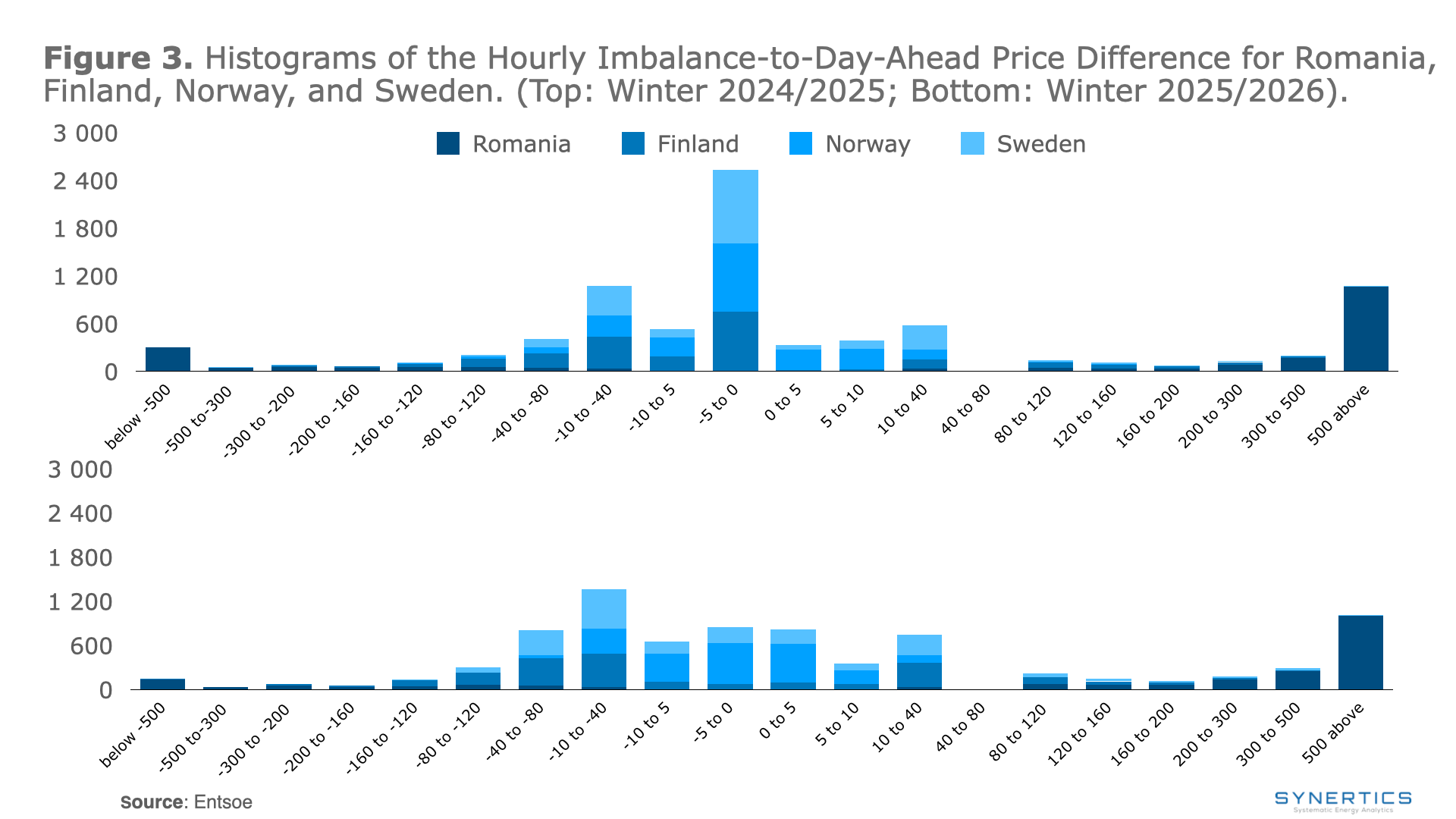

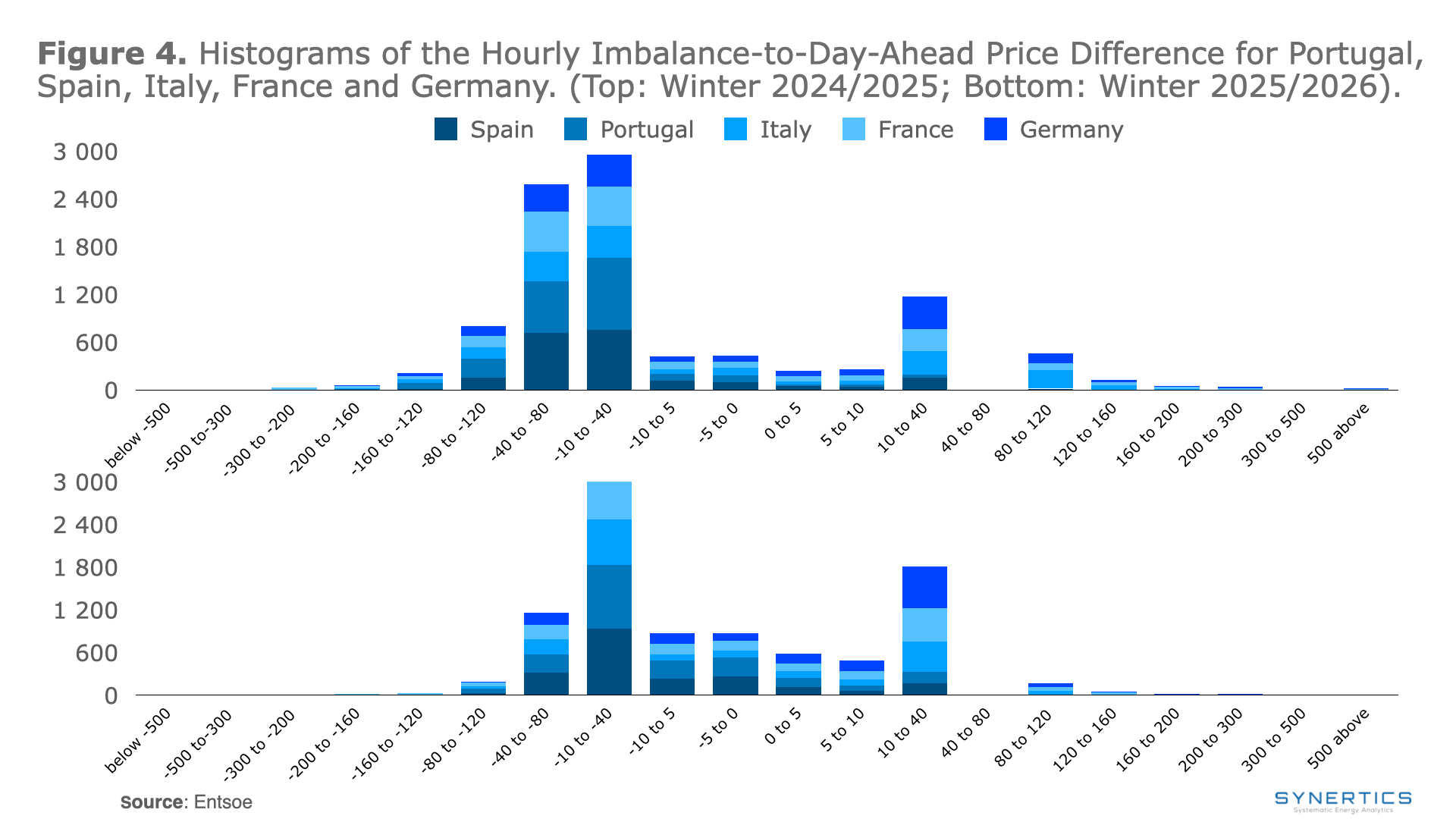

To assess the financial impact of this winter relative to the previous year, we look at the Day-Ahead (DA) market. In this market, energy producers sell their forecasted output 24 hours before delivery, allowing them to lock in a fixed price for each hourly block. While producers always receive this locked-in DA price for the volume they sold, any difference between their actual generation and their forecasted output, whether unexpected wind rops, cloud cover or equipment issues, is settled through the Imbalance market. Where imbalance prices can be highly volatile and are rarely in the producer’s favor.

Figures 3 and 4 highlight this gap, showing a comparison of this winter season of 2025/26 to the previous season. A distribution tightly clustered around zero reflects a market where forecasts were reliable and deviations are flatter and more spread out in winter 2025/26, with more hours falling into the extreme price difference buckets on both sides. For producers, every hour in those tails is a direct hit to revenue of the park.

The contrast between regions tells an important story. In South and central Europe, the storms that drove record renewable output also made generation far harder to predict. Spain and Portugal both show a notable difference between the day-ahead and the imbalance price in the -40 to -100 €/MWh range, meaning producers frequently generated less than promised and paid the price for it. Spain’s nuclear baseload provided some structural stability to the broader grid, but wind and solar producers still bore the forecasting risk individually. Romania stands out as the most exposed market, with the heaviest tail in the extreme deviation buckets, a possible reflection of this winter's volatility and deeper structural issues in how its grid manages imbalance, a trend that has been persistent since last year.

In the Nordic region, the picture is more contained but not without risk. Sweden remained the most stable of the three, with deviations largely clustered near zero, a sign of a well-integrated grid with sufficient balancing resources and the presence of high differences, mainly negative, due to possible wind droughts this year. Norway and Finland showed wider distributions, indicating an increase in the market volatility. In Finland, a 7.58% decrease in hydro generation, shown in Figure 2, significantly reduced the available balancing flexibility. Meanwhile in Norway, a decline of 4% in wind generation outweighed the small increase in hydro. These supply constraints meant that whenever wind producers overestimated their output, imbalance prices would rise to try to replace the missing energy that the market would face, resulting in a wider spread between Day-ahead and imbalance prices.

This winter's evidence points to a clear divide between technologies. Naturally, seasonal conditions made solar participation minimal and riskier. Hydropower remained the most resilient, controllable output meant operators could match their Day-Ahead (DA) commitments and avoid imbalance penalties. Wind lacked this buffer and when actual weather missed the forecasts, the financial costs were significant. Suggesting that hydro delivered where water was abundant, while wind fell short in markets most dependent on it, and producers without a balancing technology absorbed that cost directly. While this winter’s anomalies significantly increased imbalance penalties in the Nordic markets, with a lesser impact on Central and Southern Europe, future seasons are expected to remain stable if conditions return to last year’s levels.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

3 min

Insights, Announcements

29th Jul, 2026