Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

In recent years, national power systems have increasingly struggled to maintain secure grid balancing, mainly due to the rapid growth of renewable energy integration, as the rising penetration of variable generation sources places additional stress on grid stability. As a result, the market is seeing more negative pricing occurrences in the Day-Ahead (DA) and energy waste through curtailment. As producers seek to mitigate these risks by entering ancillary service markets, a key question remains: can ancillary services provide a reliable way for these parks to avoid technical and financial curtailment?

In this analysis, Synertics identifies potential countries where ancillary services may offer a viable income source by benchmarking aFRR capacity prices against DA prices.

This analysis focuses on reducing dependence on the spot market and identifying sustained revenue opportunities, focusing only on aFRR reserve prices. This fast-response service, acting within 30 seconds to 15 minutes, aligns well with the operational capabilities of renewable assets.

To better understand how the opportunities on each country's markets can vary, the study evaluates three specific countries. These locations were chosen due to their high levels of negative pricing and their distinct approaches to managing these fast-response services. We specifically analyse whether these different national frameworks create barriers for renewable energy providers looking to enter the market.

Spain is highlighted because its significant solar energy capacity heavily influences the day-ahead market, making alternative participation in capacity markets a highly viable option. Although they don’t have an internal aFRR Capacity market they have a different name which is secondary regulation reserve. This market operates in hourly blocks but carries a high entry barrier: assets must belong to a Regulation Zone. This requires individual renewable plants to be part of a larger portfolio managed by a Balance Service Provider (BSP) who aggregates the energy and handles the complex technical requirements of the TSO.

Finland is also considered because its specific generation mix, dominated by nuclear, wind and hydro, creates a Day-Ahead Market with frequent low-prices periods. This drives the need to secure revenue in other markets to decrease spot-market risk, such as the aFRR Capacity market. Like Spain, Finland utilizes hourly blocks for reserve procurement; however, the market is significantly more approachable. Finland’s regulatory framework supports Independent Aggregators, allowing smaller renewable assets and batteries to participate directly in the balancing market without being tied to the restrictive "Regulatory Zone" structures found in Spain.

The third country considered is Germany to showcase a distinct regulatory framework. This market operates in 4-hour blocks requiring providers to guarantee availability for significantly longer windows than the hourly formats. Furthermore, Germany utilises a "Pay-as-Bid" pricing mechanism for capacity, which, combined with a highly saturated market of prequalified batteries and large-scale hydro, often pushes down balancing capacity prices.

For this study, pricing data from both aFRR and DA was aggregated to an hourly resolution for consistency. The key indicator used was the difference between the aFRR capacity and the DA prices at each hour. This indicator is then examined through the distribution of all hours in 2025. To assess the proportion of time each pricing regime occurs during 2025, the distribution is divided into three categories:

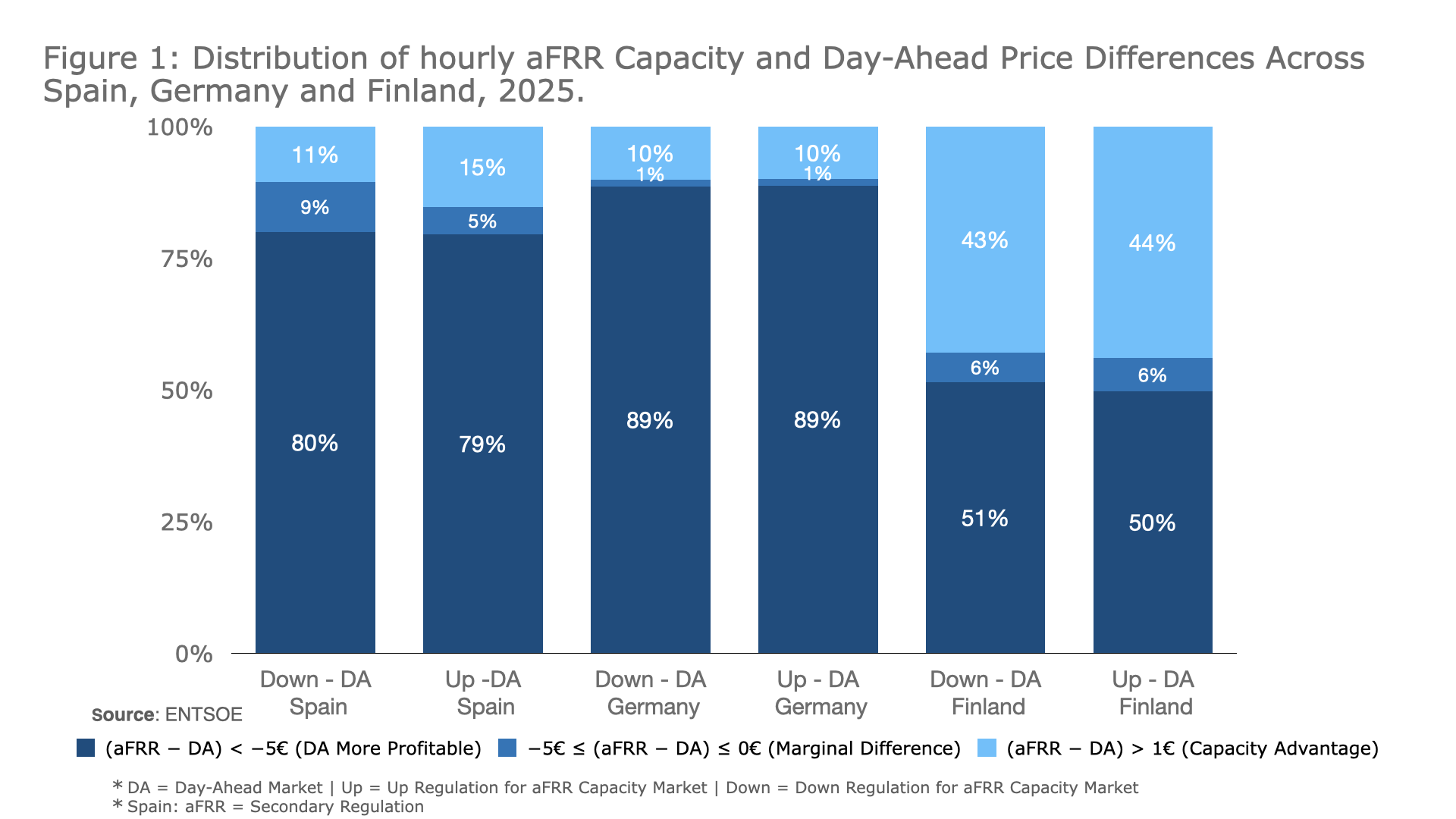

Figure 1 demonstrates that Finland is the most attractive market for aFRR services, providing a reliable alternative for producers during periods of low or negative Day-Ahead prices. For Up and Down regulations, the opportunity window was nearly 45% of the hours in 2025. This suggests that it can be due to the Finland open regulatory framework, where the freedom of this internal market for renewable assets, especially wind parks, leads to more competitiveness in this market and as the market works with marginal pricing (pay-as-cleared), the prices might rise. On top of this, the pricing dynamics is heavily influenced by the country’s generation mix. As hydro operators tend to view their reservoir water as a stored asset, rather than selling all their generation in the DA market, they would look for more lucrative balancing markets. In 2025, this included the newly automated Nordic mFRR Energy Activation and the pan-European platform (PICASSO). When this is paired with Finland’s frequent low Day-Ahead prices, driven by high wind and nuclear participation, the result is a persistent positive and near 0 €/MW difference of both markets, aFRR capacity and DA.

The same cannot be said for Spain, where the number of occurrences that there was aFRR capacity advantage, was around 11% and 15% for down and up regulation. Although it has the same hourly blocks as Finland, the possible reasons are that it has less occurrences of participating in the aFRR market. Could be due to mainly the market entry as producers need to be part of a regulation zone to participate in this market, managed by BSP’s. This has their disadvantage as not only they take a part of the revenue made but also for a preference of this market agent to other more reliable sources such as combined cycle gas turbines. Also, Spain’s low day-ahead prices are largely driven by high renewable penetration, with solar, wind, and hydro all participating in lowering prices throughout the year. During these hours, prices become highly predictable and often very low, which reduces incentives to participate in the aFRR market.

For solar and wind parks, this raises a key question: why submit a downward aFRR bid if energy bidded in the day-ahead market can already face negative prices? In such cases, reserve revenues would not be enough to cover these negative day-ahead prices. This also helps explain why upward regulation opportunities occur more often than downward regulation. Providing upward regulation does not necessarily require prior participation in the day-ahead market, making it easier for some assets to participate.

In Germany, it was the worst case, as Capacity advantage was around 10%. This could be due to the 4-hour block bidding requirement. For renewable assets, this is difficult to guarantee, as their production depends on meteorological conditions and failing to deliver what was offered lead to big fines, increasing the risk for solar and wind parks to participate in this market. Additionally, Germany’s high integration of renewables and battery energy storage (BESS) has created a more stable DA market with reduced volatility. This stability means that DA prices rarely drop below aFRR capacity prices, resulting in frequent negative spreads and only marginal positive or near-zero opportunities for producers.

As a way to reduce exposure to wholesale price volatility and avoid periods of zero or negative prices, Finland in 2025 proved to be an attractive market for participation in the aFRR capacity market, with aFRR prices exceeding day-ahead prices 40% of the time. This advantage is largely due to its more flexible participation framework. In contrast, Spain and Germany impose stricter requirements, such as regulation zones and longer commitment durations, which limit accessibility for solar and wind producers. As a result, these markets offer fewer opportunities for renewable assets to use aFRR participation as a strategy to reduce dependence on day-ahead price dynamics.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

3 min

Insights, Announcements

29th Jul, 2026