Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

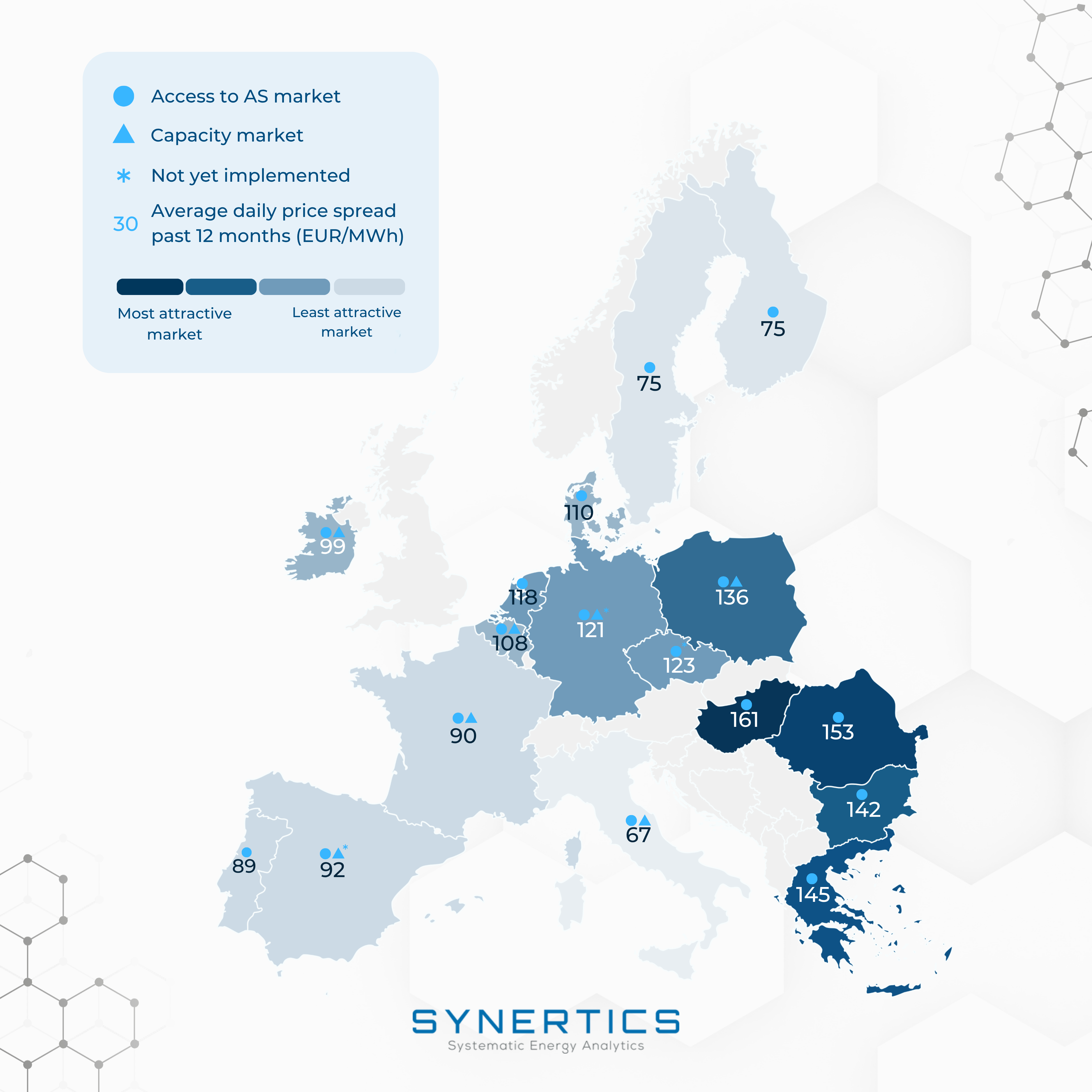

Hungary, Romania, and Greece offer the strongest arbitrage economics for battery storage in Europe, with average 2-hour daily price spreads of €160.58, €153.43, and €144.88/MWh respectively, more than double what investors can expect in Italy (€66.50/MWh).

That gap matters more than ever. BESS costs have fallen roughly 30% with each doubling of production, making the business case viable across more markets than just a few years ago. But where you deploy determines whether a project generates strong returns or marginal ones. Choosing the right country is arguably as important as choosing the right technology stack.

To identify the most attractive markets, we ranked 17 EU countries by their storage investment potential, weighting heavily on the average 2-hour daily price spread, the clearest indicator of arbitrage upside, alongside negative price hours and access to ancillary services markets.

Last updated: 29 July 2026

🇪🇺 Europe Battery Storage Potential: Key Facts (Jul 2025–Jul 2026)

Source: Day-ahead market prices (July 2025 – July 2026). Spread = avg. daily difference between highest and lowest 2 consecutive hours.

To assess the attractiveness of energy storage across EU countries, we considered the following indicators:

Average 2-hour daily price spread: Average daily price spread, the difference between the highest 2 consecutive hours and lowest 2 consecutive hours of electricity prices each day. The data used is for the last 12 months (01-07-2025 till 01-07-2026).

Number of hours with negative prices in a year. The data used is for the last 12 months (01-07-2025 till 01-07-2026).

Access to ancillary services and capacity markets: These are key for revenue stacking. However, due to data limitations, we only include basic eligibility, not detailed elements such as market maturity, payment structures, saturation levels, or bidding barriers, which also strongly affect real-world profitability.

We placed greater weight on the daily spread, as it better reflects arbitrage potential, the core revenue stream for most BESS projects. While negative prices signal oversupply and potential charging opportunities, they don’t necessarily indicate consistent profit potential. In contrast, the daily spread captures market volatility, revealing when batteries can buy low and sell high.

Southeast Europe (Romania, Bulgaria, and Greece) is a highly attractive region for BESS deployment. All three countries rank among the highest in mean daily price spread across the EU, with Romania posting the second-highest figure in the entire dataset, behind only Hungary. This price volatility indicates strong opportunities for energy arbitrage.

These elevated spreads are primarily driven by insufficient electricity interconnections in Southeast Europe, which limit the efficient transport of energy from major European markets into the region. This structural weakness creates persistent price imbalances. Although these countries have made significant investments in renewable energy to reduce their reliance on imported fossil fuels, these efforts are insufficient to offset the impact of limited transmission capacity and the inefficiencies in regional electricity markets. Recognising these challenges, the governments of Greece, Romania, and Bulgaria announced in 2024 that they would work together to develop a regional mechanism aimed at mitigating electricity price fluctuations, reflecting their view that the EU’s single market framework is ill-suited to address the specific conditions of Southeast Europe.

While the occurrence of negative prices is lower compared to Western markets, the high spreads suggest that batteries can still capitalise on significant intra-day price fluctuations. Romania’s mean 2-hour daily price spread over the last 12 months stands at €153.43/MWh, with Greece and Bulgaria following closely at €144.88/MWh and €142.40/MWh, respectively. These elevated spreads underscore the region’s potential for profitable energy storage operations.

Access to the ancillary services markets is progressing, although regulatory frameworks remain in development. Notably, Bulgaria only recently, in 2024, recognised BESS as independent market participants through amendments to its Energy Act and Electricity Trading Rules, allowing standalone and co-located storage projects to engage directly in energy trading and grid balancing activities. Overall, the fundamentals point to a promising investment outlook for storage in the region.

Central Europe (the Czech Republic, Poland, and Hungary) shows strong potential for BESS deployment, anchored by Hungary’s position as the highest mean daily price spread in the entire EU dataset, at €160.58/MWh. Poland also ranks among the top five in Europe with an average spread of €136.01/MWh, while the Czech Republic posts a competitive €122.94/MWh. These figures indicate attractive opportunities for energy arbitrage. Negative price occurrences are moderate, which supports some additional arbitrage upside.

While regulatory progress varies, all three countries have continued integrating BESS into broader energy strategies, with improving access to ancillary services. The Czech Republic has moved fastest: its Lex OZE III law, approved in March 2025, formally recognised standalone energy storage as an independent business activity, with the storage-specific provisions taking effect in October 2025 and allowing batteries to connect to the distribution grid without being tied to a generation source.

The Nordic region (Finland, Sweden, and Denmark) combines relatively low daily price spreads with a comparatively small share of negative-price hours across the EU dataset. Combined with modest average 2-hour daily spreads of €75.27/MWh in Finland, €74.81/MWh in Sweden, and €109.78/MWh in Denmark, pure price arbitrage opportunities remain limited in the region. As a result, ancillary services continue to be a key revenue stream for BESS operators here.

In Sweden, BESS deployment was limited until 2022, but recent growth has been driven by high ancillary market prices, especially for FCR-D. While market saturation is now putting pressure on FCR-D prices, this segment remains the main income stream for Swedish battery operators.

The Western European markets of Ireland, the Netherlands, Belgium, Germany, and France show daily price spreads ranging from €90.19/MWh in France to €121.16/MWh in Germany, alongside varying occurrences of negative prices and evolving ancillary service opportunities.

The Irish BESS market is experiencing substantial growth, though the regulatory backdrop is shifting under it. Most currently operational batteries were developed under the DS3 ancillary services framework, whose regulated arrangements expired on 30 April 2026. The full replacement, a competitive auction model known as FASS, isn’t expected to go live until May 2027, with an interim day-ahead system services auction targeted for December 2026 in between. Ancillary revenues are widely expected to compress once the new auction model takes hold, reshaping the calculus for operators who built their model around DS3.

Germany is one of Europe’s largest BESS markets and led the continent in new battery storage capacity additions in 2025, adding roughly 6.6 GWh as EU-wide installations hit a record 27.1 GWh for the year. Extensive participation opportunities in ancillary services continue to generate interest in the market, alongside a favourable regulatory backdrop. Germany’s power plant strategy, agreed in November 2025, targets a capacity market framework for 2027, with the comprehensive market expected to begin operating around 2032, though German BESS regulation has shifted direction multiple times over the past year, so this timeline should be treated as provisional rather than settled.

In Southern Europe, Italy, Spain, and Portugal present diverse opportunities for BESS, albeit with generally lower mean daily price spreads: Spain at €92.44/MWh, Portugal at €88.97/MWh, and Italy at €66.50/MWh.

Italy’s strong commitment to expanding renewable energy has created important opportunities for BESS, with investors mainly relying on two key mechanisms: long-term auctions like MACSE and shorter-term Capacity Market auctions. The MACSE programme, managed by grid operator Terna, offers 15-year contracts that provide high revenue certainty, making it particularly well-suited to southern Italy where abundant renewable resources coincide with weaker grid infrastructure.

In contrast, the Capacity Market auctions, more common in the industrialized north, provide shorter-term opportunities aligned with the region’s robust infrastructure and higher electricity demand. Given that Italy also operates a zonal electricity market, the location of BESS installations is therefore a critical factor influencing their financial performance and choice of strategy.

Spain has announced ambitious renewable expansion plans and has seen increased interest in BESS deployment since the April 2025 Iberian Peninsula blackout. Progress had lagged due to the absence of a clear and comprehensive regulatory framework, but the European Commission approved a €9 billion, ten-year capacity mechanism for Spain in May 2026, covering generation, demand response, and storage. Operational rules and the first auctions are still being finalised, so the mechanism’s practical impact on BESS revenue remains to be seen.

Based on our comparative assessment, Central and Southeast Europe emerge as the most attractive regions for new BESS deployment, together accounting for four of the five highest average daily price spreads in the EU dataset. Hungary posts the single highest spread overall, with Romania, Greece, and Bulgaria close behind, driven by exceptionally high daily price spreads that create strong arbitrage opportunities. However, this promising outlook comes with important caveats, as the long-term attractiveness of BESS projects depends on a much more complex interplay of factors. These include the country’s electricity generation mix, grid capacity and interconnectedness, market saturation levels and the robustness of national regulatory frameworks. Consequently, investors should carefully weigh these fundamental market and policy considerations to ensure sustainable and resilient returns on battery storage investments.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

4 min

Insights, Market-trends

12th Jun, 2026

8 min

Insights, Market-trends

11th Jun, 2026