Join us on our journey towards renewable energy excellence, where knowledge meets innovation.

In this article, we will provide an in-depth overview of the Power Purchase Agreement (PPA) market in Germany, exploring the key factors driving its growth and transformation. We will delve into Germany's ongoing renewable energy expansion and the growth of the PPA market. Alongside this, we will examine regulatory changes, such as the shift from feed-in tariffs to competitive auctions, and their impact on renewable energy projects. Additionally, we will explore crucial market indicators, including capture prices, futures markets, imbalance costs, and grid curtailments, which are significantly influencing PPA negotiations. This overview will give you a comprehensive understanding of the current PPA landscape in Germany.

🇩🇪 Germany PPA Market: Key Facts (2025)

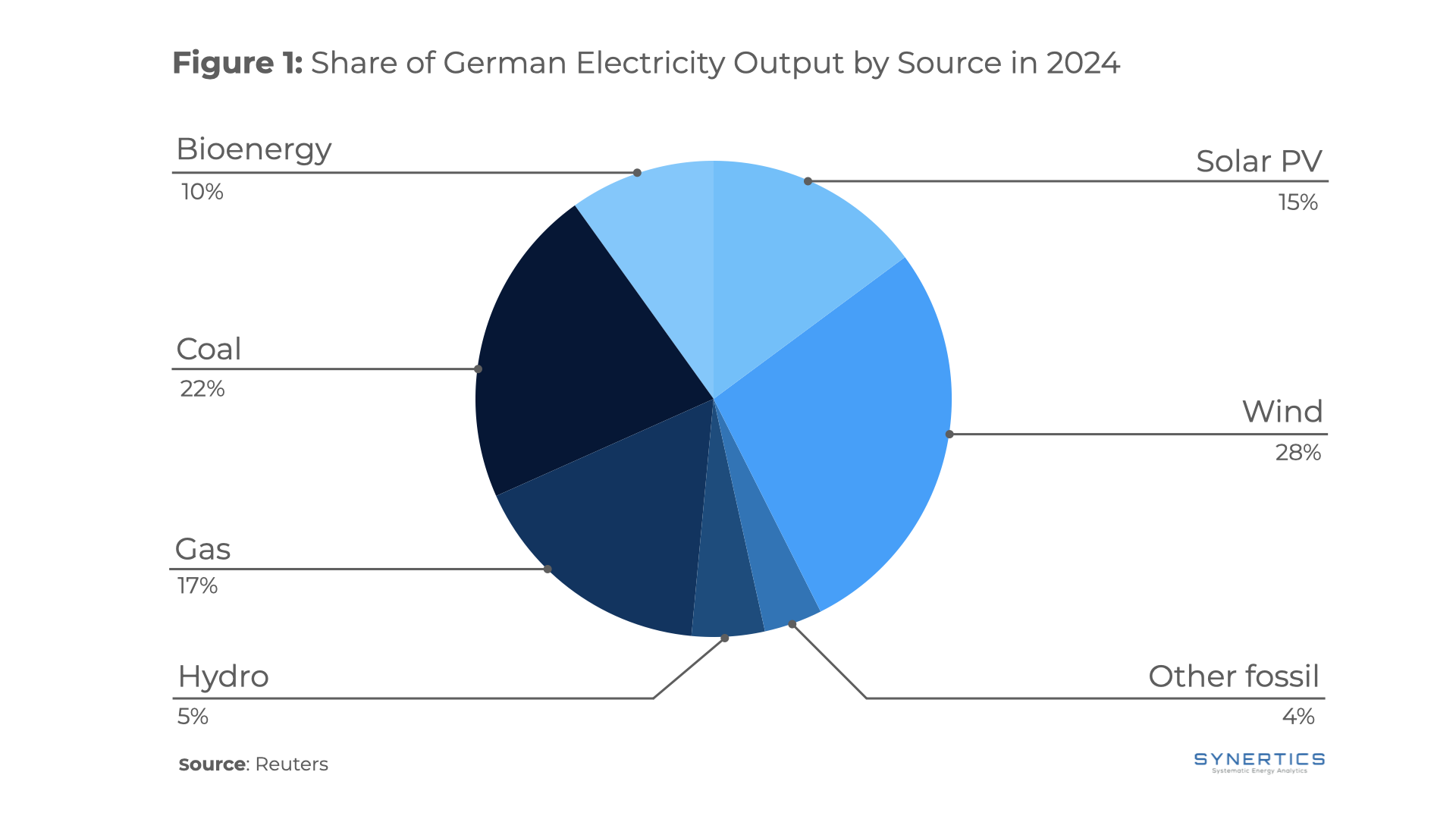

Germany’s electricity mix has undergone a significant transformation in recent decades. In 2024, wind power is the country’s largest source of electricity, accounting for 28% of total generation, followed by coal at 22%. Solar PV contributes 15%, while bioenergy makes up 10%. Gas, hydro, and other fossil sources account for 17%, 5%, and 4%, respectively.

Germany’s shift toward renewables has been particularly notable, with wind and solar making up a combined 39% of electricity generation—three times the global average. This puts Germany on par with other leading renewable energy adopters such as Spain (40%) and the Netherlands (41%). The country’s reliance on coal has declined dramatically, from 52% of electricity generation in 2000 to just 22 % in 2024. This transition has driven a significant reduction in power sector emissions, which peaked in 2007.

Germany made significant progress in expanding its renewable electricity capacity in 2024, adding nearly 20 GW—a 12% increase from the previous year—bringing the total to just under 190 GW. Solar energy led this growth, with a record 16.2 GW added, increasing total solar capacity to 99.3 GW. Onshore wind expanded by 2.5 GW (net), reaching 63.5 GW, and received record-high approvals for 15 GW of future capacity. Offshore wind added 0.7 GW, doubling its growth from the previous year and bringing the total to 9.2 GW. Biomass continued its steady growth, increasing by 110 MW to a total capacity of around 9 GW.

Germany is committed to reaching net zero emissions by 2045 under its Climate Law and has set ambitious renewable energy targets. By 2030, the country aims to generate 80% of its electricity from renewable sources and reach 100% by 2035 while phasing out coal entirely. Following its nuclear exit in 2023, Germany is accelerating renewable energy expansion, with legislative reforms supporting the growth of onshore wind to 100–110 GW, offshore wind to 30 GW, and solar to 200 GW by the end of the decade.

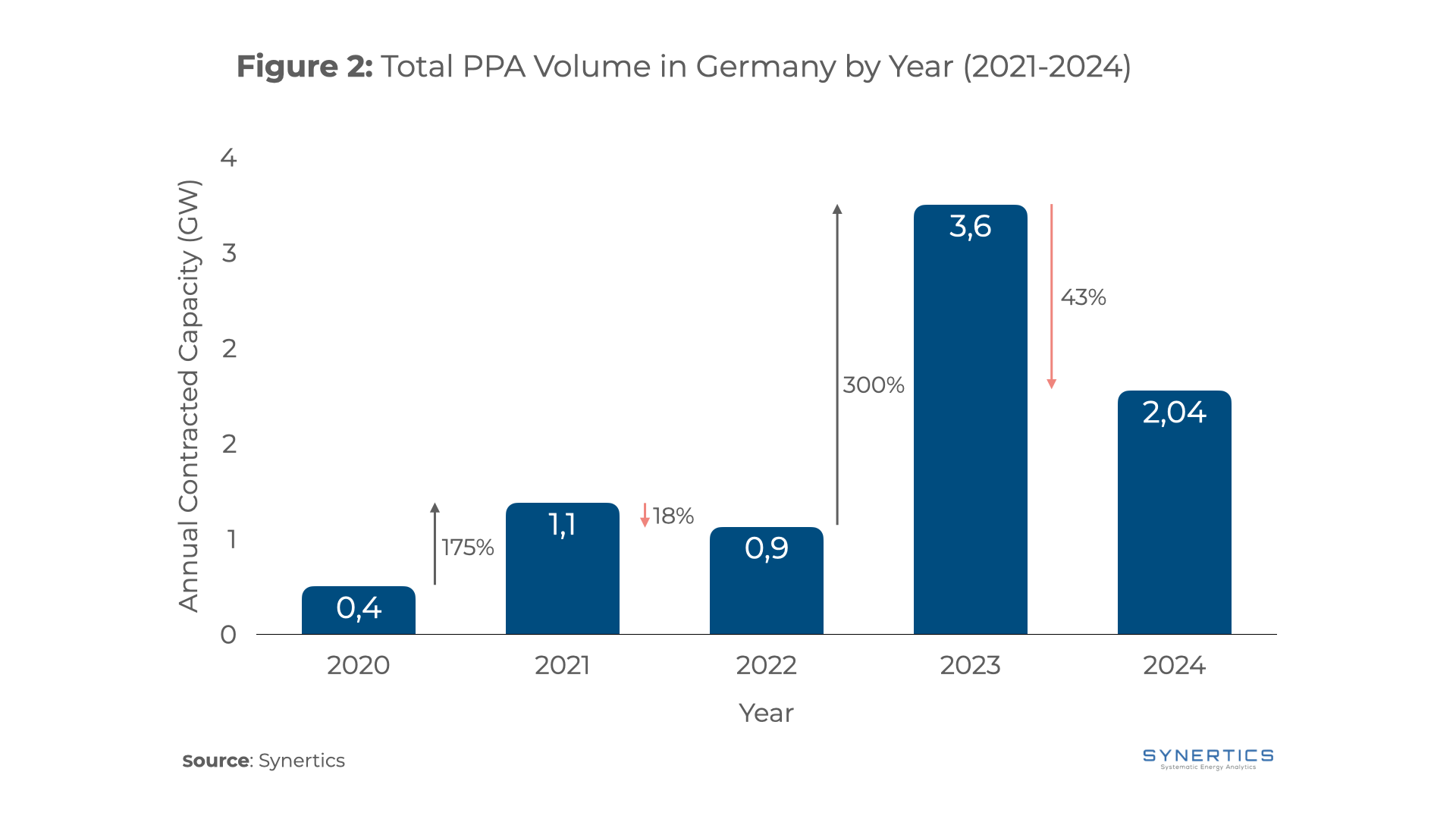

Germany currently has the second-largest PPA market by contracted capacity in Europe, only surpassed by Spain. The market has evolved significantly over the past few years, with a mix of solar and wind deals driving growth. From 2020 to 2024, there has been a steady increase in the number of agreements. These agreements range from small local rooftop solar projects to large-scale offshore wind deals, showcasing the market’s expanding scope.

In 2020, Germany's PPA market began recovering from the initial disruptions caused by COVID-19. Solar power dominated the activity, with the total contracted volume reaching 0.4 GW. Precise figures vary by source and definition, but estimates suggest corporate PPA contracts in 2020 amounted to 300–500 MW.

The German PPA market surged in 2021, growing by 175% compared to 2020, reaching 1.1 GW of contracted capacity. This sharp increase was largely driven by the expansion of wind PPAs, particularly among industrial players looking to secure long-term price stability.

The momentum slowed slightly in 2022, with contracted capacity declining by 18% to 0.9 GW. This dip was mainly due to price volatility and broader economic uncertainty, which caused some PPA negotiations to stall. In total 23 PPAs were signed in 2022.

2023 marked a turning point for the German PPA market, with contracted capacity skyrocketing by 300% to 3.6 GW, making it the most significant year to date. This surge was largely driven by corporate compliance with new reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) and a broader push for net-zero targets. This expanded ESG reporting obligations from 500 to 15,000 companies in Germany. Additionally, there was a notable increase in solar PPAs, which accounted for nearly half of the volume, with 1.8 GW of new contracts. A total of 42 PPAs were signed, nearly doubling the 23 PPAs signed in 2022.

While 2024 saw a 43% decline in contracted volume compared to the record-breaking 2023, Germany remains one of Europe’s most active PPA markets, reaching 2.04 GW of newly signed agreements. Key trends include a continued focus on solar PPAs, with major deals shaping the early months of the year. One of the largest agreements so far includes a 208 MW solar PPA signed in April. There was also a rise in deal count, with Germany recording 48 long-term PPAs, a 9% increase year-on-year. This indicates that while the total contracted volume declined, the number of deals signed increased, pointing to a shift toward smaller-scale agreements. As companies of all sizes seek renewable energy solutions beyond traditional large-scale infrastructure projects, the growth in deal count reflects an increasing demand for smaller, more flexible PPAs, rather than a focus on large, high-volume contracts.

Germany’s Renewable Energy Act (EEG) has played a crucial role in shaping the country’s renewable energy market and has undergone significant changes over the years. Originally introduced on 1 April 2000, the EEG built on the Electricity Feed-in Act of 1991, which was the world’s first green electricity feed-in tariff scheme. The early EEG guaranteed a grid connection, priority dispatch, and government-set feed-in tariffs for 20 years, funded by a surcharge on electricity consumers. This policy spurred rapid growth in wind and solar energy.

However, as renewables gained a larger share of Germany’s electricity mix, rising from 3.6% in 1990 to 30% in 2015, the system evolved to introduce more market-based mechanisms. A major reform in 2014 marked a shift towards competitive auctions for large-scale renewables, replacing fixed feed-in tariffs with a market premium model. This transition was fully implemented under the EEG 2017, which established annual capacity targets through competitive tenders.

Under this auction system, renewable energy projects no longer receive a guaranteed tariff but must bid in government-run tenders to secure financial support. Only projects that win an auction receive funding, ensuring cost efficiency and better grid integration. The key elements of the auction system include:

Effects of switching from Feed in Tariffs to Auctions

The shift to a competition-based market premium under EEG 2017 has significantly reduced subsidy levels due to increased competitive pressure, which has led to a decline in funding rates across all renewable technologies. This trend is expected to continue in the future, forcing some renewable energy technologies to focus less on EEG funding and more on selling electricity through alternative mechanisms. For instance, the average price for ground-mounted solar PV in 2004 was 457 EUR/MWh, but by 2012, it had dropped to 187.6 EUR/MWh. In the most recent 2025 auction, the average bid value has further decreased to 47.6 EUR/MWh.Similarly, the price for onshore wind in 2012 was 89.3 EUR/MWh, while the latest auction in 2025 shows a further reduction to 70 EUR/MWh.

The auction system has also created another challenge. Oversupply of bidders has become a common feature of the tenders, increasing competition among developers. For instance, in the latest onshore wind auction, a total of 506 bids were submitted, representing a bid volume of 4.9 GW. In total, 422 bids with a capacity of 4 GW were awarded. A similar trend was seen in Germany’s latest solar PV tender, where bids exceeded the auctioned total capacity by more than twice. Nearly 5 GW of projects were submitted, but the Federal Network Agency (BNetzA) ultimately awarded 242 projects with a total capacity of 2.15 GW.

Impact on PPAs

This situation presents a significant opportunity for PPAs. As EEG subsidies continue to decline and competitive auctions leave many projects without financial support, developers are increasingly turning to alternative revenue models. PPAs allow renewable energy producers to secure long-term contracts with industrial and commercial buyers, providing financial stability without relying on government-backed mechanisms.

The publication of a standard PPA contract for the German market by the Renewable Energy Market Offensive provides much-needed support for smaller companies and municipal utilities looking to secure long-term green electricity supply. By simplifying the contracting process and incorporating key elements of German law and electricity trading, the template lowers barriers to entry for organizations lacking in-house expertise. This initiative not only facilitates broader PPA adoption but also strengthens market participation, enabling more businesses to benefit from price stability and decarbonisation while contributing to Germany’s renewable energy expansion.

For developers interested in selling Guarantees of Origin (GOs) in Germany, it is important to note that the country’s Doppelvermarktungsverbot law (literally: “double sale ban”) prohibits renewable energy assets receiving subsidies from issuing GOs. This rule is designed to prevent asset owners from benefiting twice, once through government support and again from selling GOs. Since subsidy payments currently exceed the potential revenue from GO sales, most asset owners choose not to participate in the GO system.

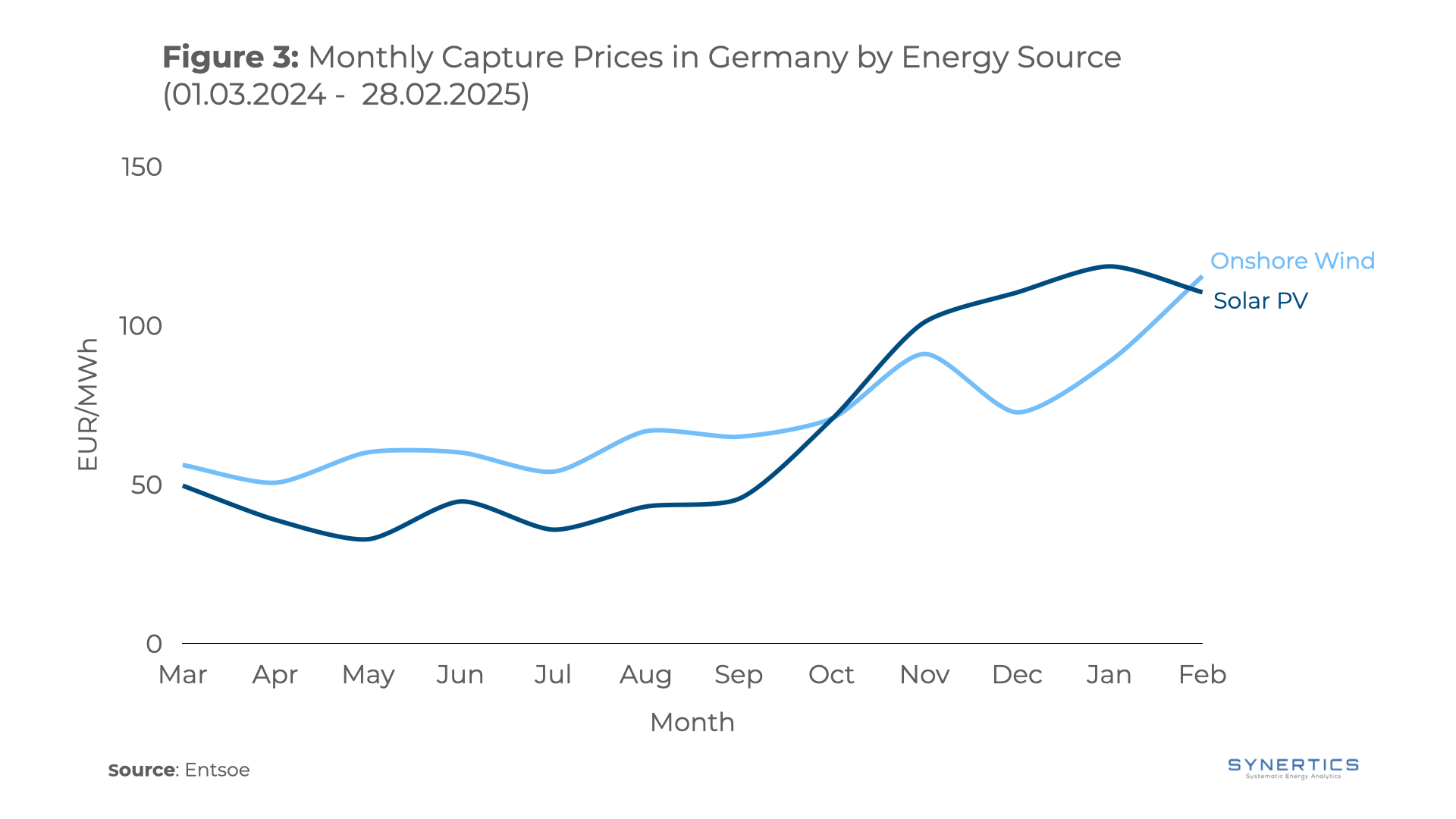

Germany’s renewable energy sector is facing significant shifts in capture prices for renewable projects, especially for solar PV. The record of PV generation following a surge in installations has led to price cannibalisation, where high solar output during peak periods suppressed market prices. Such a phenomenon can be especially seen in summer months, where the capture price for the technology reached values as low as 35,72 EUR/MWh in July. Wind generation, although typically better remunerated, still suffers from the high solar production mimicking the solar price curves, as depicted in Figure 3. This dynamic had repercussions on tender prices, leading to lower bid prices, reinforcing the need for PPAs for generators to secure competitive and long-term price revenue streams.

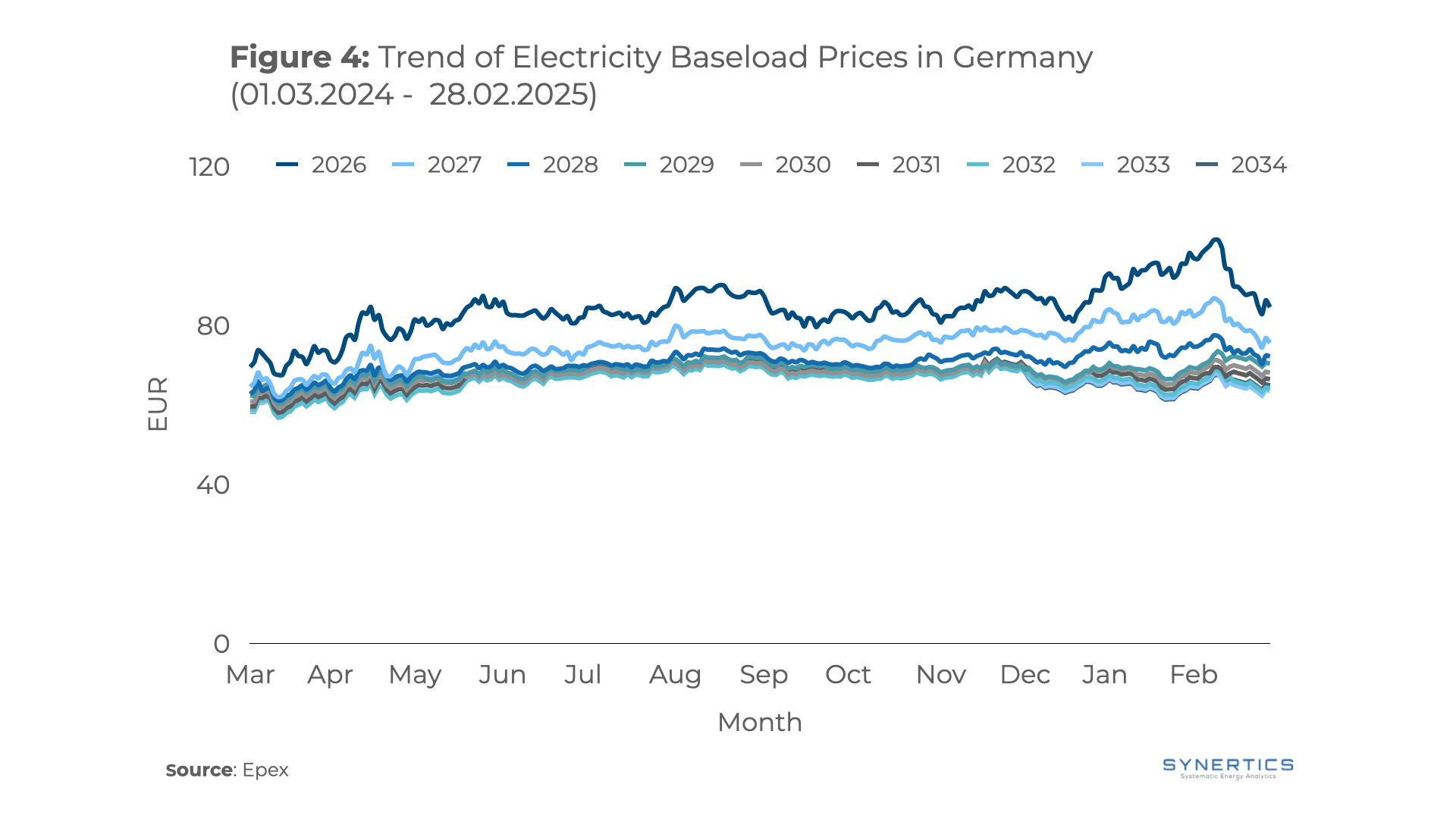

Germany has a highly liquid electricity market, with futures traded up to 10 years ahead. This liquidity provides market players with valuable insights into long-term electricity price expectations.

Over the past few months, Germany’s baseload power futures have experienced significant fluctuations, as seen in Figure 4. The ongoing energy crisis following geopolitical tensions and supply disruptions marked the futures markets across all of Europe, and Germany was no exception.

Prices peaked in mid-February but have since declined sharply. This downward trend poses additional challenges for generators, as baseload futures are closely tied to capture prices, exerting further downward pressure on revenues.

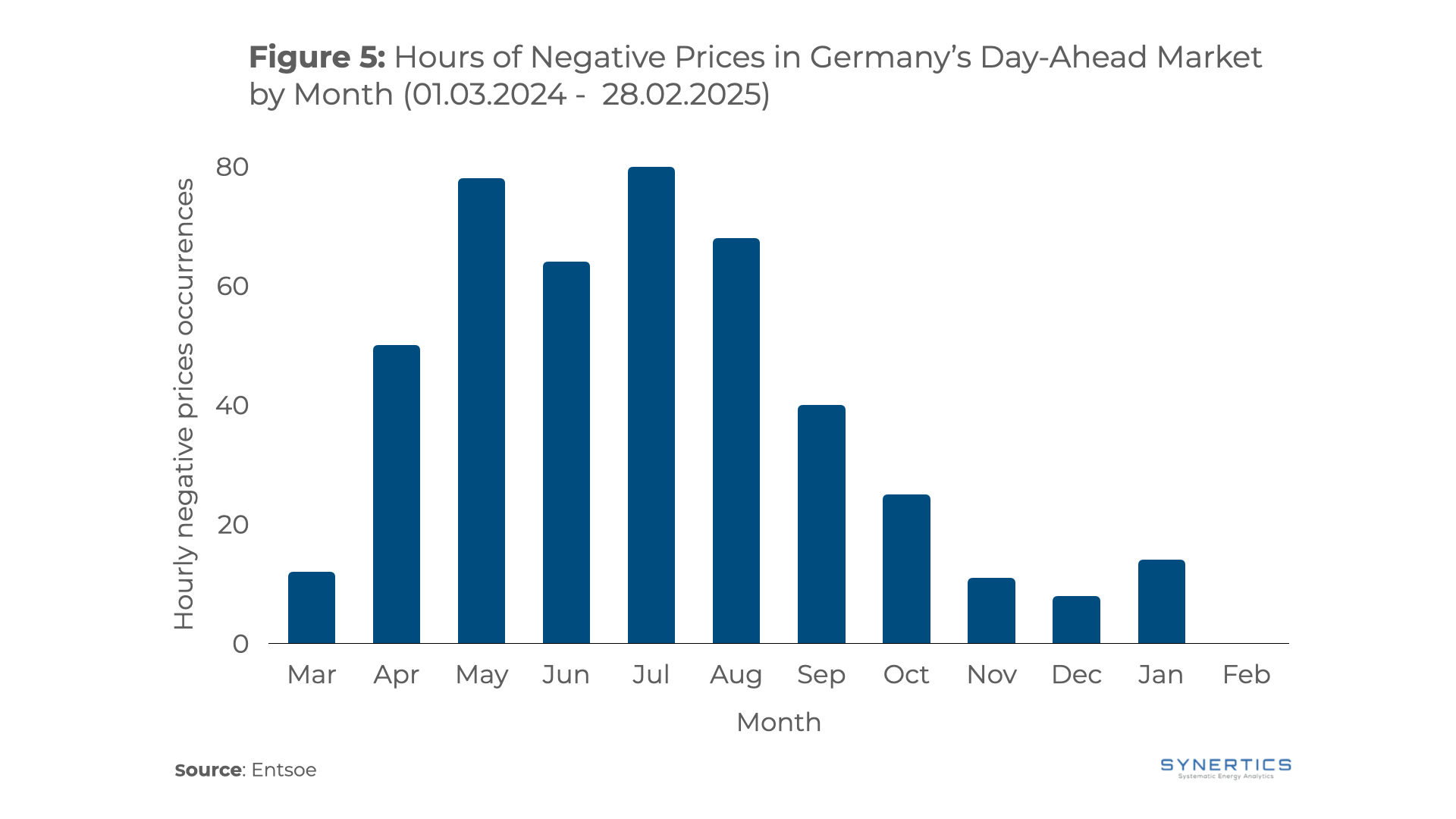

The surge in negative prices has become a key factor in PPA negotiations. Over the past year, Germany set a new record with 457 hours of negative prices, highlighting the challenges posed by the rapid expansion of solar PV. As shown in Figure 5, these occurrences were most frequent during the summer months when solar production peaks. This issue is becoming increasingly relevant for lenders, as addressing price volatility is essential for securing financing for renewable projects.

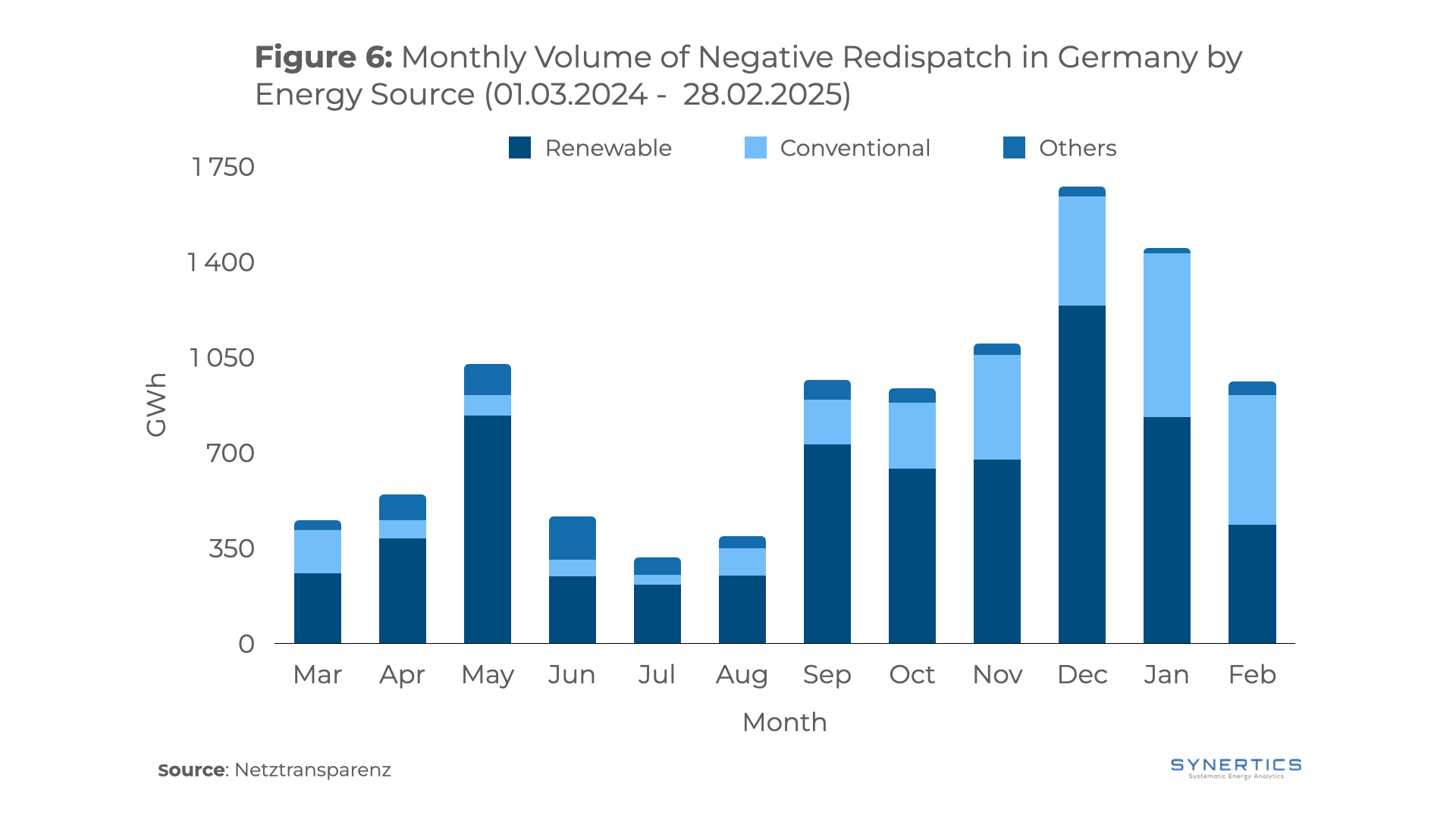

In recent years, Germany has faced increasing challenges with electricity grid congestion, leading to the curtailment of renewable energy sources, particularly wind power. The geographical imbalance, as the majority of wind power is generated in the northern regions, while much of the energy-intensive industries are concentrated in the south, leads to significant levels of curtailment, with renewables being significantly affected. Figure 6 illustrates the dominance of renewables in negative redispatch, with the highest volumes being reached during the winter months when the wind production is at its peak.

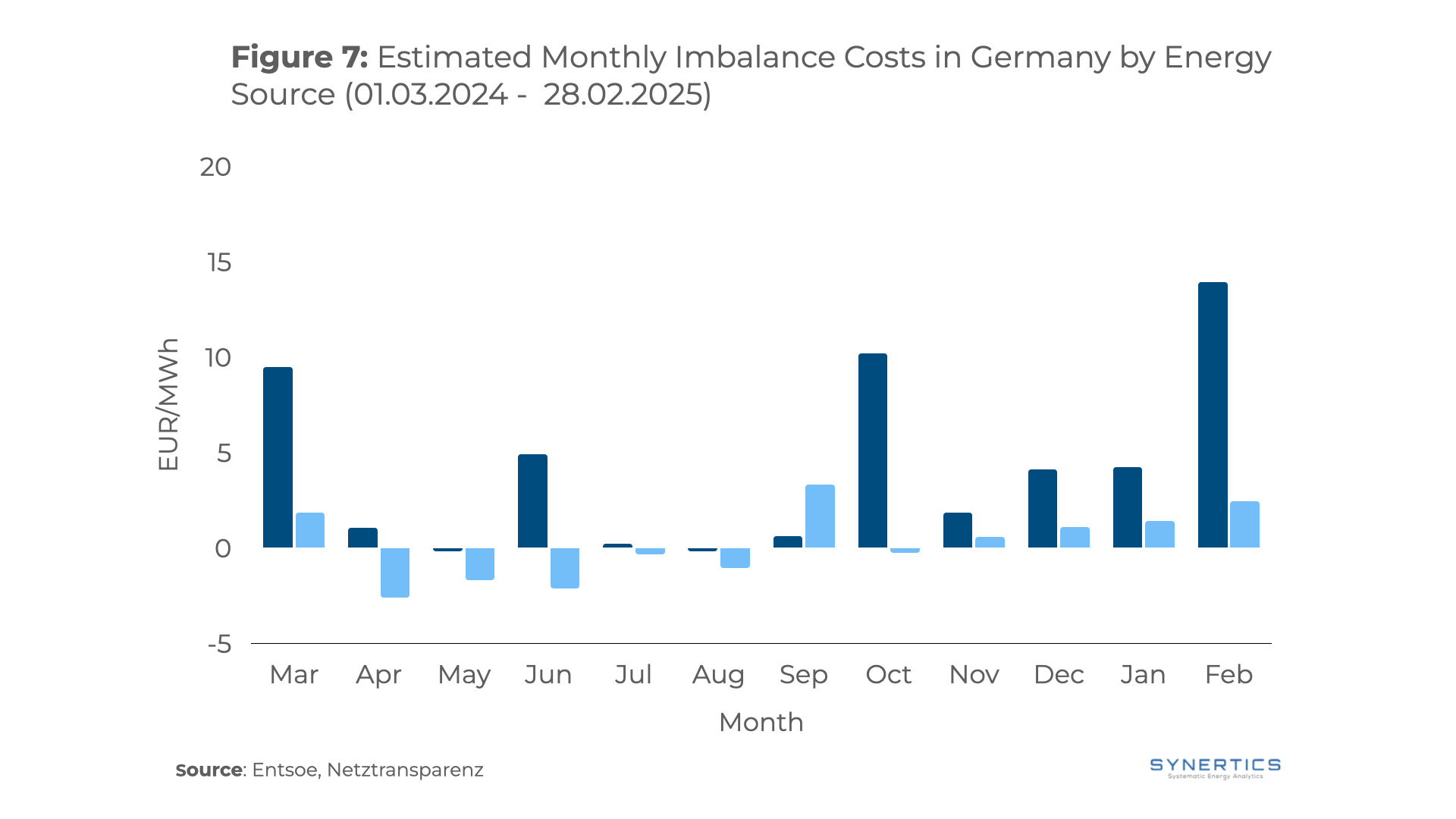

Imbalance costs are a significant expense for renewable energy generators. Deviations between expected and actual production force generators to cover the shortfall or excess by trading imbalance volumes in the imbalance market. This market reflects the higher system costs incurred by the transmission system operator (TSO) due to the activation of additional resources to maintain grid stability.

By analysing the gap between expected and actual generation by technology and country, along with imbalance market prices, we have estimated the average costs incurred by generators, as shown in Figure 7 below. Notably, solar generation exhibits higher imbalance costs. This is primarily due to its production peaking simultaneously across large areas, requiring greater system capacity to maintain balance.

In summary, Germany’s renewable energy sector is undergoing significant changes, driven by shifts in the PPA landscape, evolving regulations, and market dynamics.

The PPA market in Germany has experienced substantial growth, particularly for solar and wind power, with an increasing number of corporate buyers seeking long-term contracts to meet their sustainability goals. From small-scale local projects to large offshore wind deals, the PPA market is expanding across various sectors.

Germany’s Renewable Energy Act (EEG) has played a key role in the development of the country’s renewable energy market. The shift from feed-in tariffs to competitive auctions under the EEG 2017 has resulted in declining subsidy levels for renewable projects, leading developers to seek alternative revenue models like PPAs. While auctions have increased market efficiency, they also increase competition, with many projects not receiving government support. This drives a larger reliance on PPAs to ensure financial stability.

Lastly, the market is experiencing significant price fluctuations, particularly in capture prices. Negative pricing, especially during solar peaks, and the growing imbalance costs, primarily affecting solar generation, highlight the need for developers to secure long-term, stable revenue sources. Grid curtailments, due to congestion, further emphasise the risks faced by developers in the current market. PPAs offer a solution, providing price stability and financial security amid these market pressures.

With these challenges and opportunities, it is clear that PPAs are becoming an essential tool for renewable energy developers in Germany. At Synertics, we are committed to helping you navigate these complexities and optimise your PPA strategies. Reach out to us today to learn more about how we can assist you in securing long-term success in Germany’s renewable energy market.

5 min

5 min

Insights, Market-trends, Announcements

30th Jul, 2026

3 min

Insights, Announcements

29th Jul, 2026

3 min

Insights, Announcements

29th Jul, 2026